On January 20th, 2022 I wrote a short post suggesting $100 oil could be in our future. Just over a month later I was right. (Sometimes it happens.)

In the business of investing you only need to be right 51% of the time to make a living. Let your winners ride and limit your losses.

Today I’m predicting $150 oil by the end of the summer. I don’t think it will last, however.

I could be totally wrong, but hear me out. (Please note that none of this is advice.)

The only thing stopping $150 oil, in my opinion, is a comprehensive resolution to the Ukraine invasion. One that quickly opens the door to Russian oil again. That seems quite unlikely at the moment. Russia is successfully annexing eastern Ukraine and building a land bridge to Crimea and the Black Sea, which is of critical strategic benefit. They have no reason to stop at this point.

The Russian economy appears to be holding up better than expected too. The Ruble has appreciated against the dollar and - in the face of lower exports to EU - Russia is strengthening economic ties with China and India. Russia will be a shadow of its former self, but the oligarchs will be OK. In fact, with $120 oil (even though Ural oil sells at a discount), banned imports and demand for energy payments in Rubles, Russia’s terms of trade have actually improved during this war.

What Russia lacks now is Western knowledge and goods, which are critical to Russian energy production. I doubt few alive today will see the West export strategic goods or intellectual capital to Russia again.

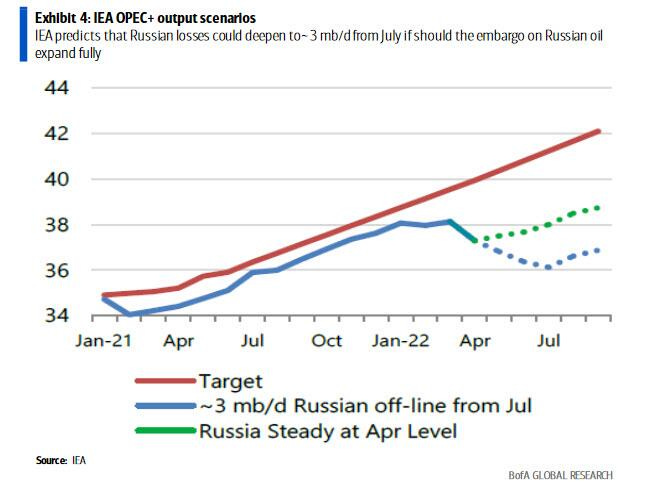

The West is increasingly distancing from Russia and sanctions could soon remove from the market around 3 million barrels per day of Russian oil. But without Western know-how, production shut-ins could permanently halt even more Russian supply over the long run.

Russia isn’t the only reason oil prices could hit $150.

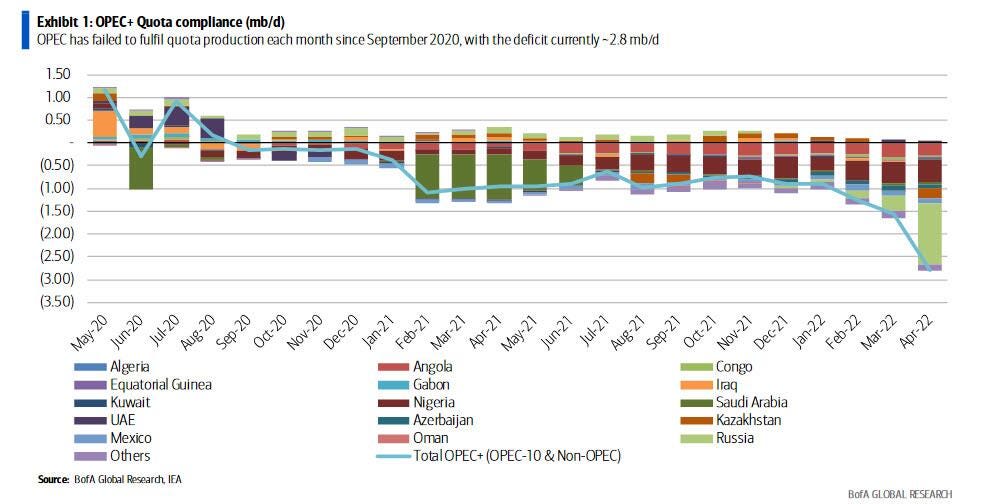

It appears that OPEC+ is running low on capacity. While OPEC makes headlines by claiming it will increase production by 648,000 barrels per day for the next 2 months, the reality is OPEC is simply bringing forward already planned month 3 production (spreading it over month 1 and 2). Before the announcement they planned to produce an additional 1.296 million barrels over 3 months. Today, they still plan to produce an additional 1.296 million barrels…just sooner.

Why won’t OPEC+ make a real commitment to supply the market? After all, they can do so at fantastic prices.

Maybe they don’t because they can’t. Or perhaps they’d rather keep the market tight, knowing that US shale production is waning and they won’t need to worry about market share for much longer.

For whatever reason, OPEC overcompliance (chart below) - whether you include Russian cuts or not - remains massive and spare capacity (upstream and downstream) is tight. Something’s not right. Whatever the reason, this is bullish for oil.

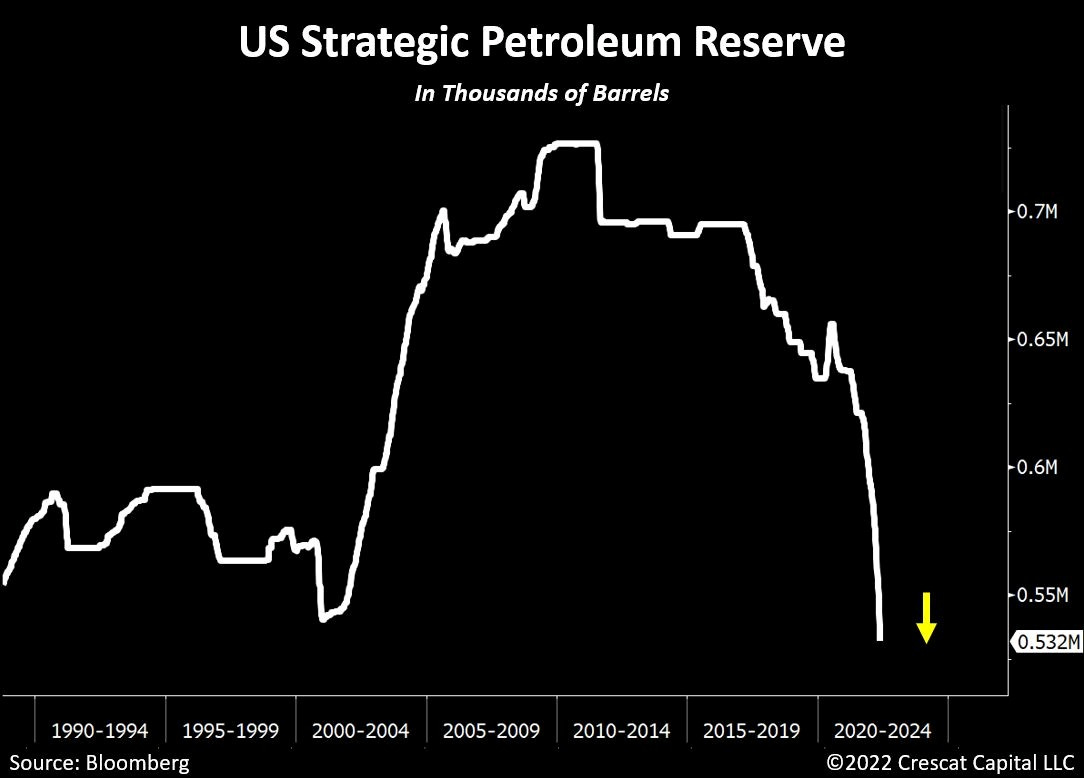

To fight high prices, the US administration is releasing 1 million barrels a day from its Strategic Petroleum Reserve (SPR). When announced, oil prices temporarily fell below $100 but quickly recovered.

The SPR is now at the lowest level in 20 years (chart below), as the US administration attempts to put a lid on oil prices. But the reserve is needed for strategic purposes - times of war, physical shortfalls - so it must eventually be refilled. Each barrel released is a barrel that must be bought back in the future. This is bullish for oil prices.

Getting oil out of the ground isn’t the only issue. The world has a shortage of refining capacity to convert crude oil into usable products. This is demonstrated by the 3-2-1 crack spread (chart below), which has recently skyrocketed.

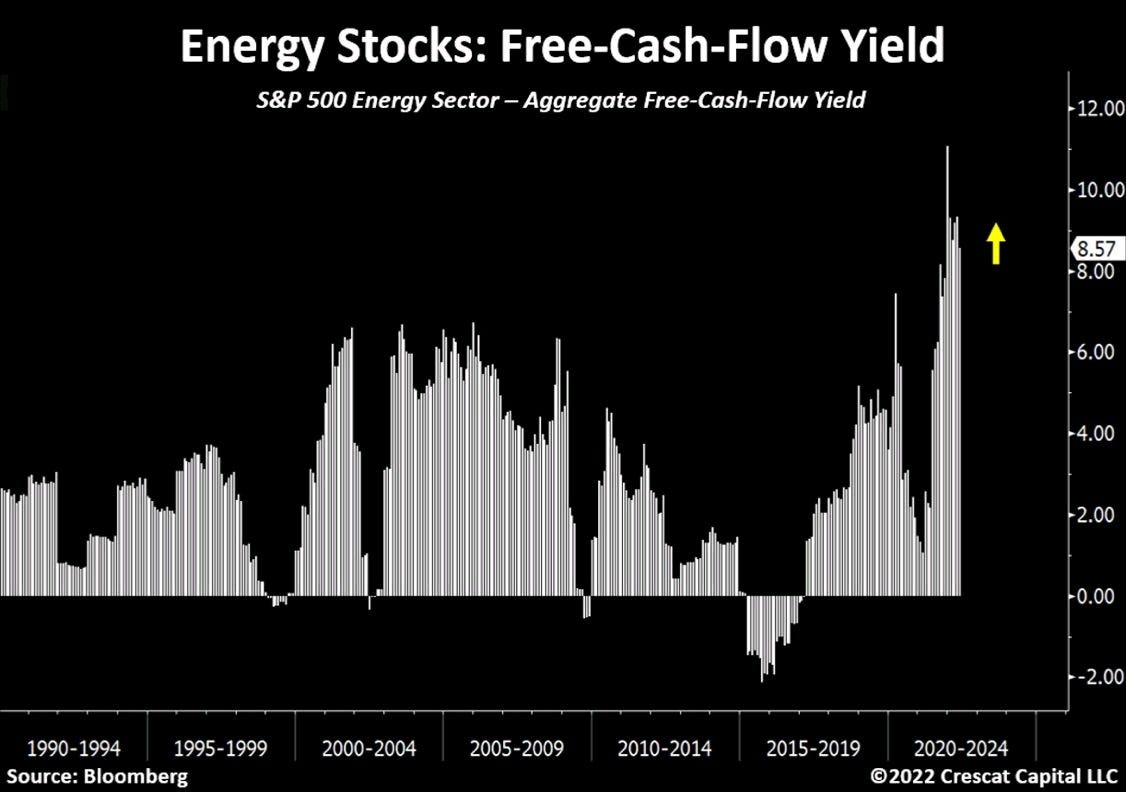

Energy companies are huge beneficiaries of higher oil prices and wide crack spreads. The free cashflow yield for the S&P 500 energy sector hasn’t been higher in more than 30 years. In fact, energy companies are more profitable today than during the commodities super cycle that ended in 2008.

In 2008, energy prices peaked at $147 bbl and subsequently crashed, alongside most other assets. The inflationary impulse building into 2008 was deadened by tightening financial conditions and weakening purchasing power. Soon enough, everything was laid bare as the financial system approached the brink of collapse, sending oil prices plummeting.

This should sound remarkably familiar. Today, many of the same underlying conditions, motivations and effects exist. The Federal reserve has made it clear that inflation is enemy #1 right now and IT WILL NOT STOP tightening the financial screws until inflation breaks. That will likely mean breaking the economy at the same time. So while I think we could see $150 oil by the end of the summer we could see much lower prices by the end of the year.