25 Charts of the Week

Massive, sudden spike in Fed's balance sheet:

Performance of various types of stocks during WWI and the Spanish Flu. "Smaller stocks with high yields (value) tend to not offer protection during these sharp market corrections but perform well during the recovery phase."

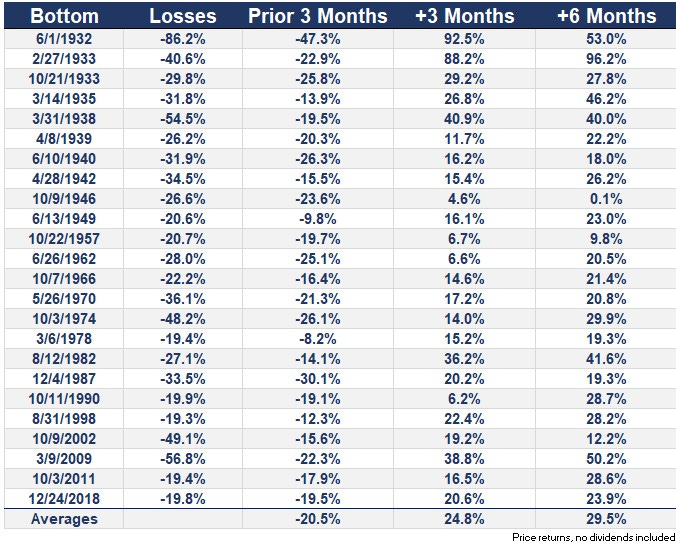

What do the returns look like in the 3 months before stocks bottom in a bear market?

2020 unemployment line is just getting started, but it will probably rival that of the Great Recession:

The worst market crashes tend to see a huge drop in earnings but the relationship isn’t perfect:

This recession will force GDP onto a lower growth path:

Slow productivity growth followed the last recession:

Fiscal stimulus needed to offset coming drop:

Students graduating in 2020 will be permanently impacted:

The data tables below show what happened across a variety of asset classes after the last four market crises. There is some variance depending on asset class and the nature of the crisis, but again, the story is uniform in the only

important respect: the markets recovered what they lost and grew nicely from there.

As of March 26, the FTSE Canada Long Corporate Bond Index yielded 3.96%, compared to the FTSE Canada Universe Bond Index yield of 2.10%, resulting in a yield advantage of 1.86%:

Big drop in manufacturing activity coming to Canada:

List of the companies and institutions developing new tests for COVID-19:

Performance of gold vs. gold miners:

The insane daily volatility of March 2020 indicated the market was broken:

In March 2020, investor sentiment sunk to levels not seen since the Global Financial Crisis. While some use this as a contrarian indicator, note how long negative sentiment in 2008/2009 persisted. In fact, the sentiment was deeply negative in EARLY 2008, prior to the near-collapse that started in September. So I question the idea that extreme sentiment is actually a contrarian indicator:

When the traditional 60/40 portfolio failed:

"Pandemics have effects that last for decades. Following a pandemic, the natural rate of interest declines for decades thereafter, reaching its nadir about 20 years later, with the natural rate about 2% lower had the pandemic not taken place. At about four decades later, the natural rate returns to the level it would be expected to have had the pandemic not taken place. These results are staggering and speak of the disproportionate effects on the labor force relative to land (and later capital) that pandemics had throughout centuries."

Pandemics also have the effect of raising real wages for some time:

Bear market rallies during the dot-com collapse and global financial crisis:

Canadian housing prices expected to take a minor hit, but quickly recover. Is this realistic? Possibly, provided flexibility is afforded to mortgage holders so they aren't forced to sell: