6 Charts Pointing to Deflation

Hard to imagine today but signals are quietly emerging

If you’re new here, DumbWealth is a no-holds barred newsletter that shares investing and career insights and charts you won’t get from mainstream sources.

Recently, most of focus is on the current economic breakdown, but during normal times I also provide tips on building wealth while beating the corporate system.

Will the Response to Inflation Cause Deflation?

We are currently in the middle of an inflationary episode not seen since the 1970s. Central banks have been slow to respond, but are now catching up. The contractionary response is becoming increasingly aggressive and central banks have told us they’re not going to stop until they achieve their goals.

The Fed’s stated goal is 2% inflation, but it is highly unlikely they get anywhere near this without first tipping the economy into recession, causing inflation to overshoot to the downside.

Is this realistic? Below I’ve shared 6 charts that suggest our next major challenge could be deflation. Why should you care? Because deflationary shocks tend end badly for the markets and employment.

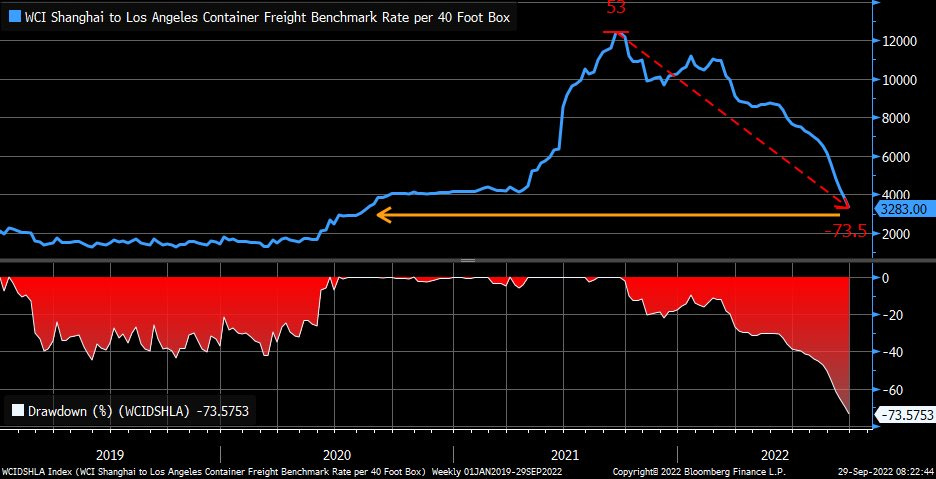

1: Shipping rates from Shanghai to LA have plummeted since the pandemic peak. While this is an indication of a healing supply chain, it is also a symptom of weakening demand.

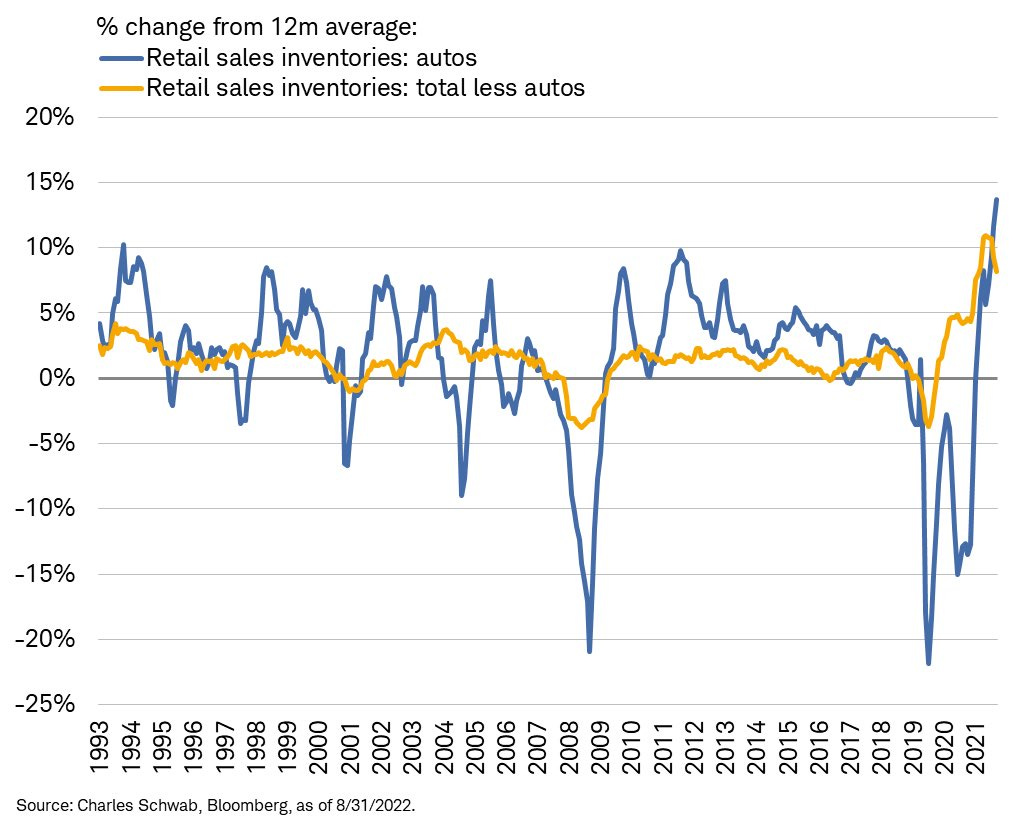

2: Automobile inventories are growing very quickly. It could soon become a lot easier to negotiate better car deals. This is great for car buyers, but indicative of easing inflationary pressures on prices due to growing inventories.

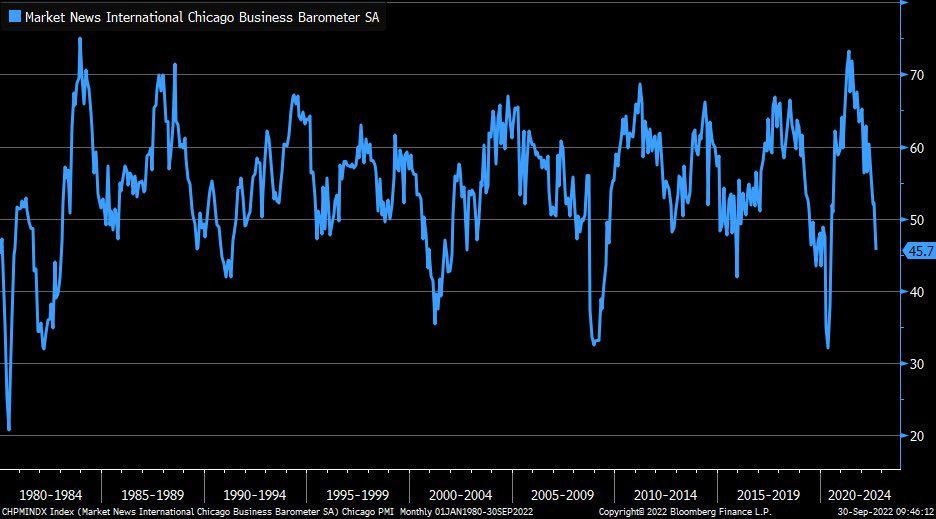

3: Chicago PMI - which measures business activity in the Chicago area - is at 45.7, which is contraction territory. Businesses are likely finding themselves overstocked with inventory they must now liquidate.

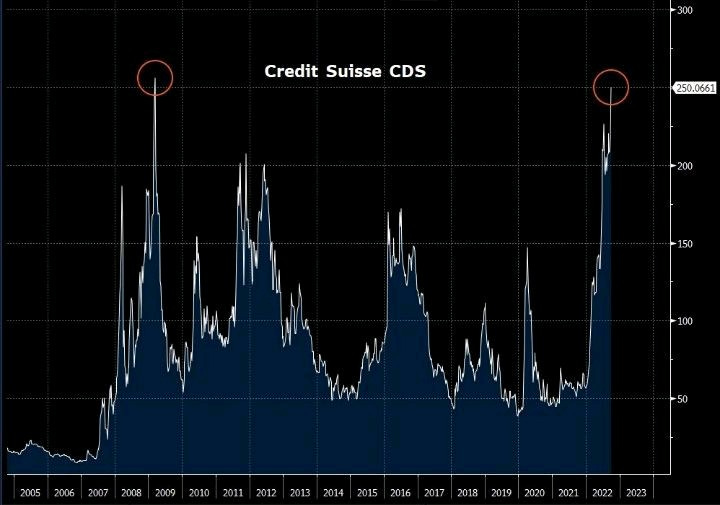

4: Credit Suisse credit default swaps (essentially, insurance on its bonds) are priced at levels not seen since the global financial crisis. European banks are under tremendous stress, and any shock brought on by bank stress could spread across the financial system, tightening credit even further.

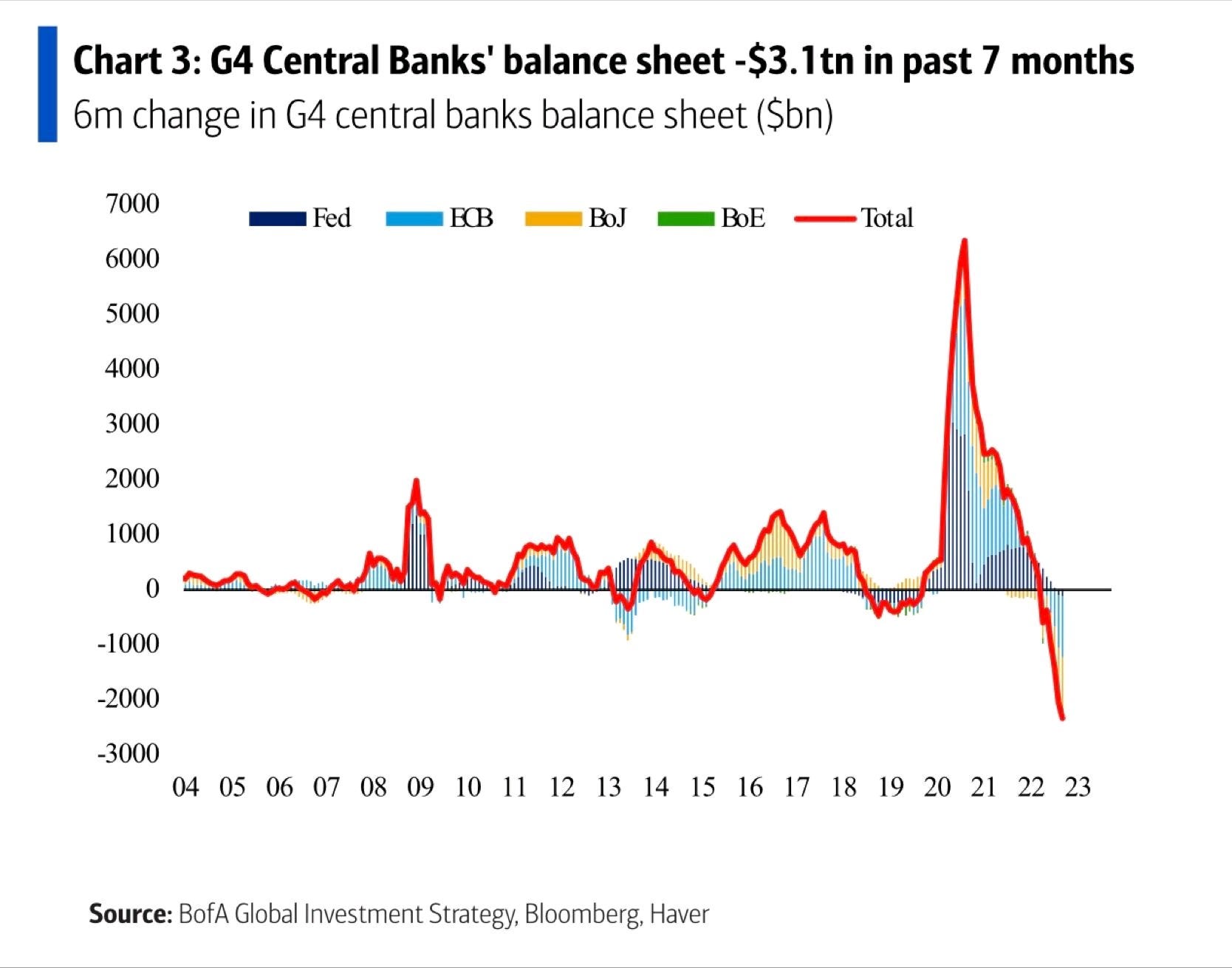

5: Global central bank action is highly coordinated and rapidly sucking liquidity out of the system. While central banks are understandably being criticized for being too expansionary for too long we should not ignore the determination of central banks to regain credibility. Today the op-eds are all about inflation, but in 12 months we might be criticizing central banks for being too restrictive for too long.

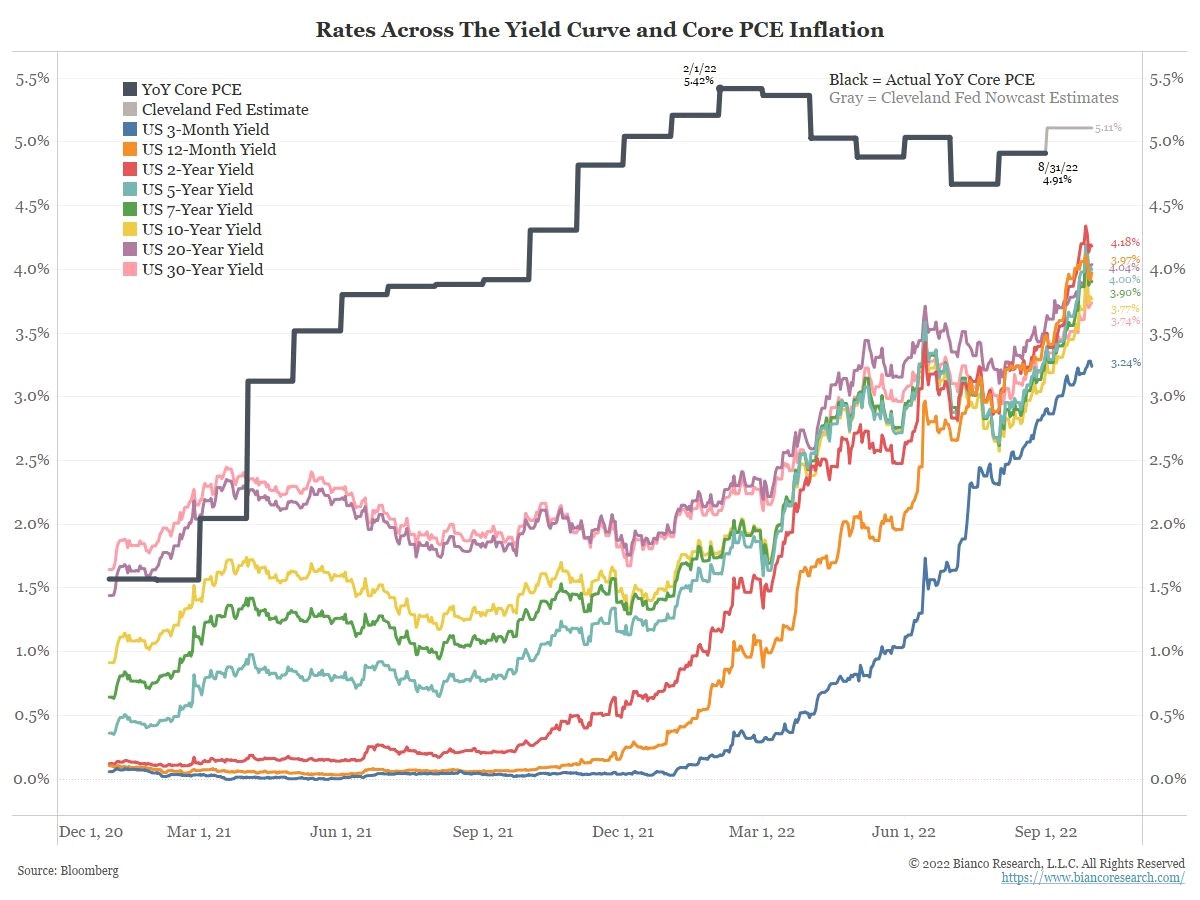

6: Why will central banks go too far? While rates are catching up, they are still below core PCE (one of the Fed’s favourite inflation metrics). In other words, real yields are still negative and the coordinated response by central banks will continue for some time.