Alarm bells are ringing

The signs are bad

I don’t mean to sound alarmist but I guess I’m getting alarmed by what’s happening in the commodities markets.

Over the past couple weeks, commodity prices have gone through the roof. The inflation we just experienced over the past 18 months appears to be worsening as conflict is creating supply risks across everything from oil to potash to wheat. This exacerbates the supply issues caused by the pandemic (global supply chain) and last summer’s heat domes (agricultural output).

What happens in remote regions of the world impacts global commodity prices. I’m particularly concerned about rising food and energy prices, due to their inelastic nature and far-reaching influence on society.

High gas prices affect elections. Hunger starts revolutions.

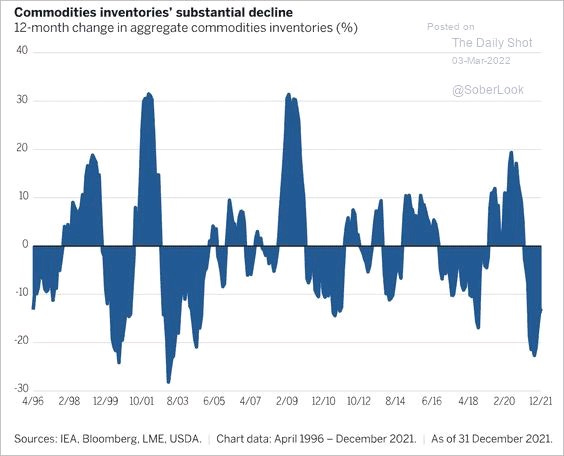

1: Commodities inventories were declining rapidly BEFORE the start of the Russian-Ukraine war. The chart below shows inventory changes to the end of 2021. Current supply issues are bound to weaken inventories even more.

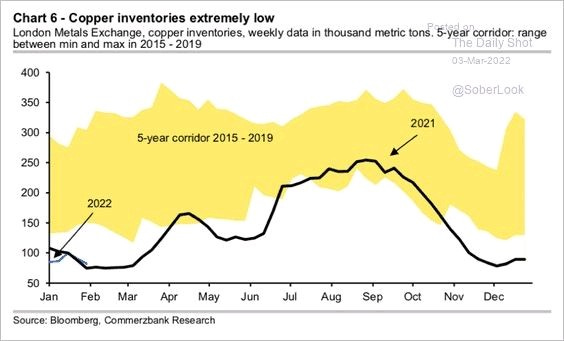

2: Looking at copper in particular, this year’s inventories are far below the recent historical range (look at the bottom-left of the chart to see how 2022 is tracking vs the yellow band).

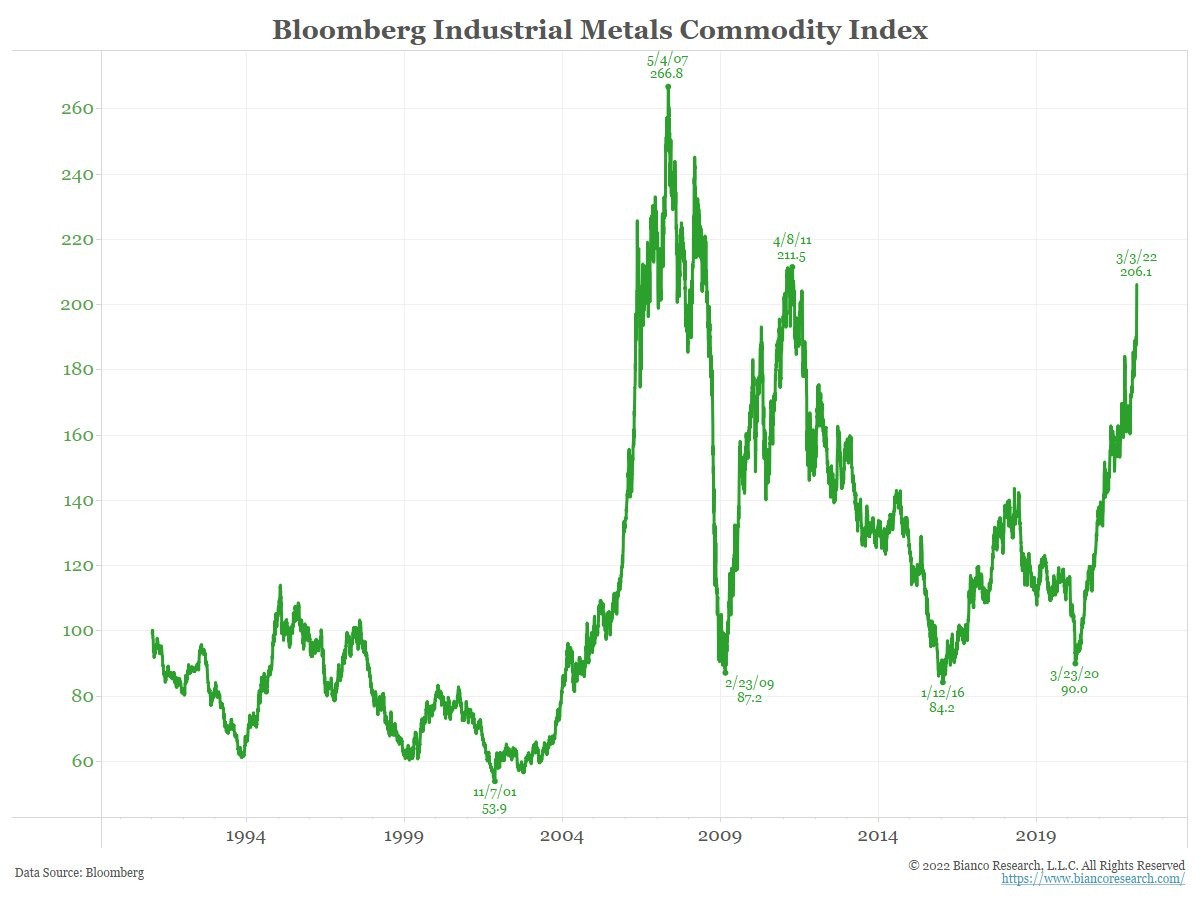

3: Consequently, metals prices are skyrocketing. (So is wheat [second chart] - Russia and Ukraine supply about 25% of the world’s wheat.)

At the same time, the value of the US dollar is rising against a basket of currencies. Since commodities are priced in USD, this means the actual cost in local currency terms is rising even faster for most non-US global citizens than what’s displayed in the financial media.

4: There will come a tipping point. At some point prices will reach a level that the market cannot bear and we will enter a recession - possibly a staflationary recession (high inflation, weak growth). Policy response during a staflationary recession is severely limited.

Indications suggest economic weakness might already be finding its way into ISM readings. This could in turn negatively impact corporate earnings in the near future.