Another blow to the US housing market

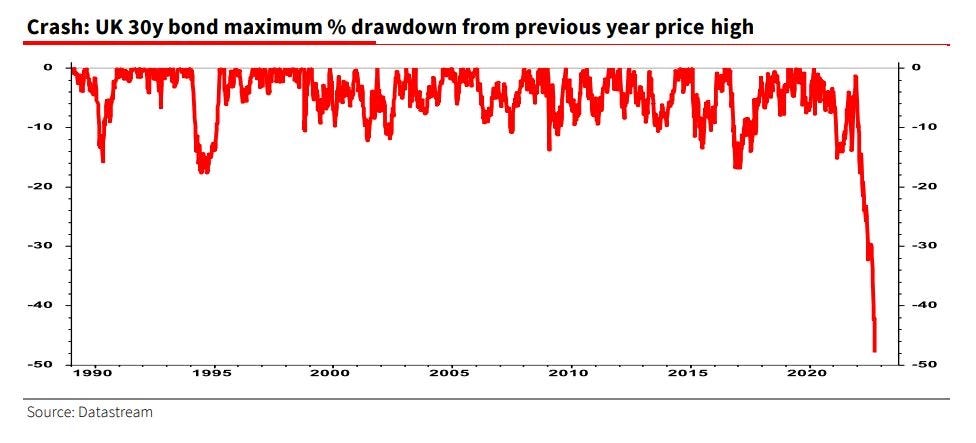

Also, UK's near pension collapse

Quick take from me, as I’ve been thoroughly exhausted the past couple days…

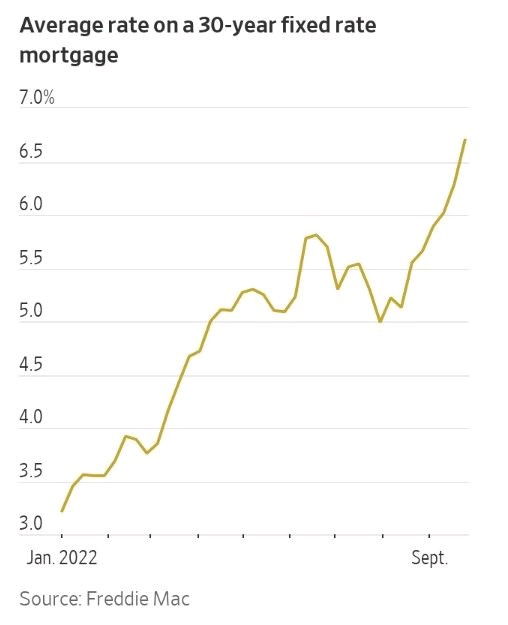

1: Another blow to the US housing market, 30 year fixed mortgage rates are quickly approaching 7%. Affordability is getting wrecked and new buyers are likely to remain on the sidelines. Many renters will keep renting and young adults will remain living with their parents.

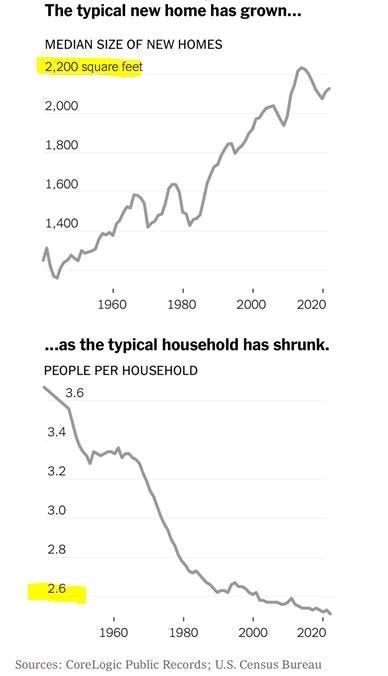

Moving out used to be a rite of passage for young adults, but things are changing and I think more people will stay with their parents well into their 20s and even 30s. People simply can’t afford to live on their own. Housing - and the middle class lifestyle in general - has become increasingly unaffordable over the years, and recent inflation has only made it worse.

Luckily, houses are getting bigger so there’s plenty of room at mom and dad’s house (second chart below).

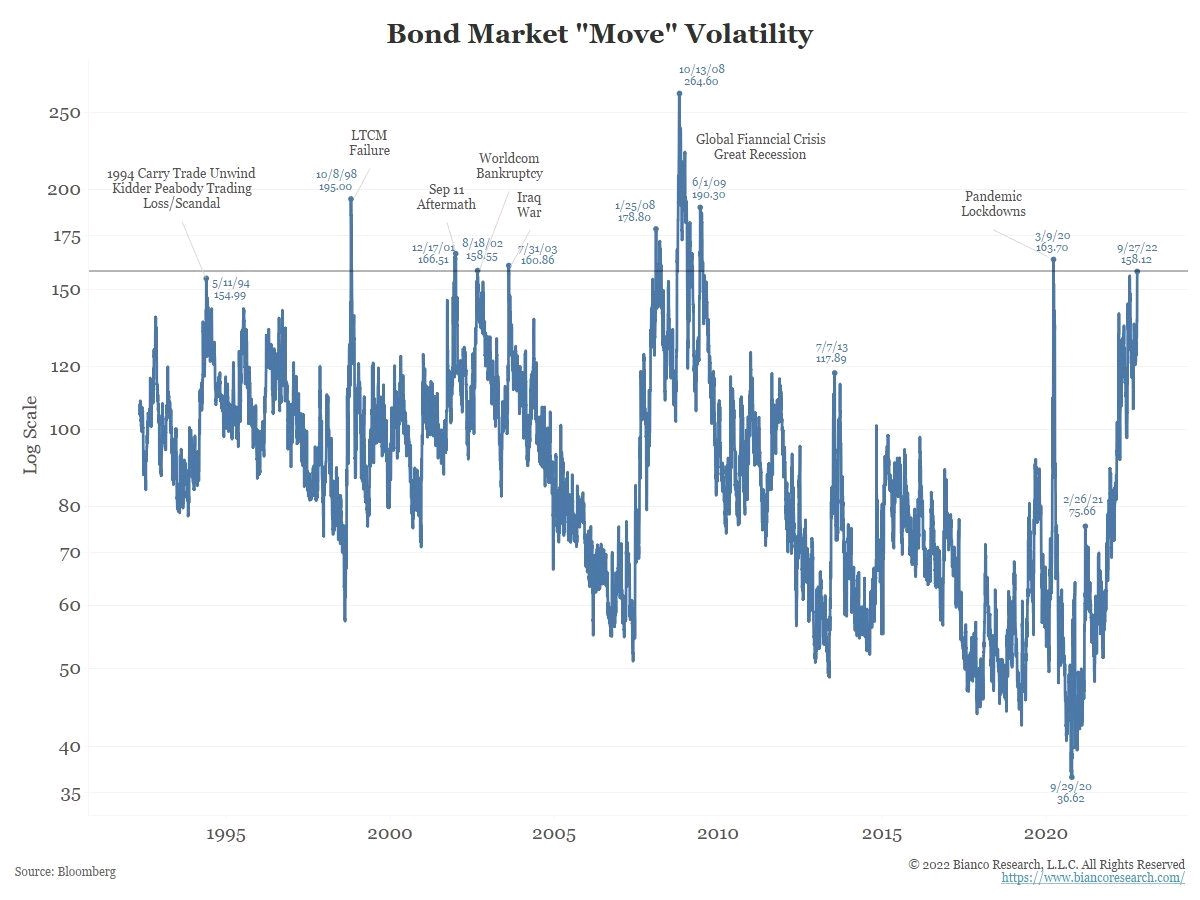

2: Many are aware that bonds have performed poorly this year. What many don’t know is bond market volatility (as shown by the MOVE index - second chart below) has skyrocketed.

This level of volatility has historically led to, or coincided with, market crises. Just this week, the Bank of England had to intervene in its bond market (QE) to drive down yields and avoid a pension system collapse.

“If there was no intervention today, gilt yields could have gone up to 7-8 per cent from 4.5 per cent this morning and in that situation around 90 per cent of UK pension funds would have run out of collateral,” said Kerrin Rosenberg, Cardano Investment chief executive. “They would have been wiped out.”

Many pundits have highlighted the contradictory nature of the Bank of England’s intervention, given its recent efforts to calm inflation. Yet, many have entirely missed the reason why they made this rapid reversal of policy. The UK came close to financial crisis this week.

The situation in the UK demonstrates how central banks are attempting to balance two forms of financial disorder: inflation and market stability.