Economic and Market Charts

Quick hits you must see

1: The gap between 10yr and 1yr Treasury yields has been decidedly negative for weeks.

According to Wells Fargo, “when this spread turns negative for at least four weeks or the curve inverts by more than 25 basis points, we view this a strong indication that a recession is likely within the next 12 months (all other factors remaining the same).”

They continue…

“Our favored yield curve inverted the week of July 11, more than four weeks ago; as of August 12, it has inverted by more than 40 basis points. We believe this inversion is a strong indicator that a recession is likely within the next 12 months.”

in advance of a recession. The relationship historically then turns positive as the recession begins and steepens as we exit a recession. Recessions are indicated by shaded areas in chart. Currently the relationship remains inverted, signaling a potential recession ahead.")

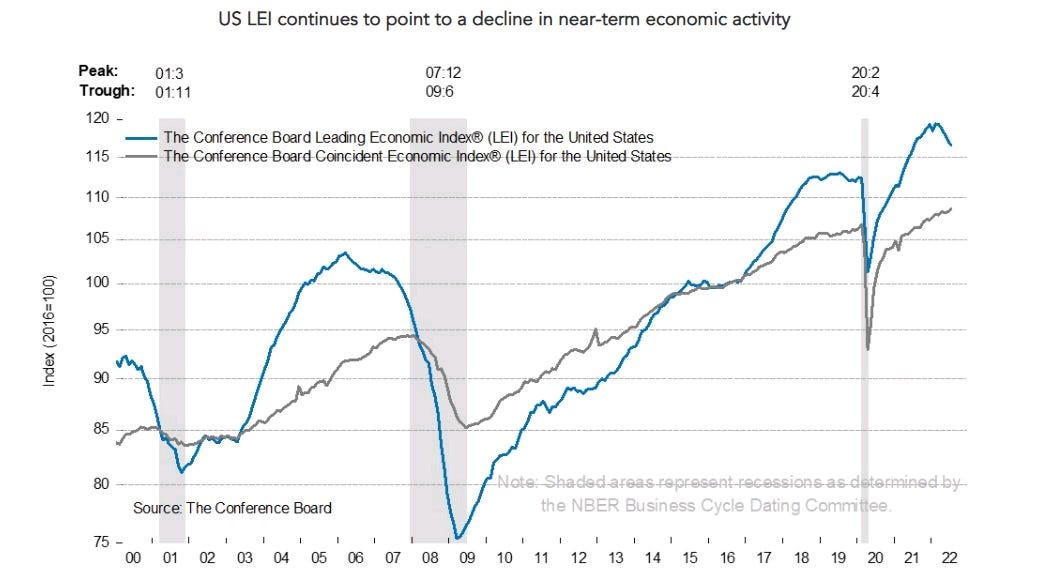

2: Economic data continues to present a mixed outlook. Hard landing vs soft landing? Leading economic indicators continue to point to a significant decline. ISM release on September 1 will be the one to watch.

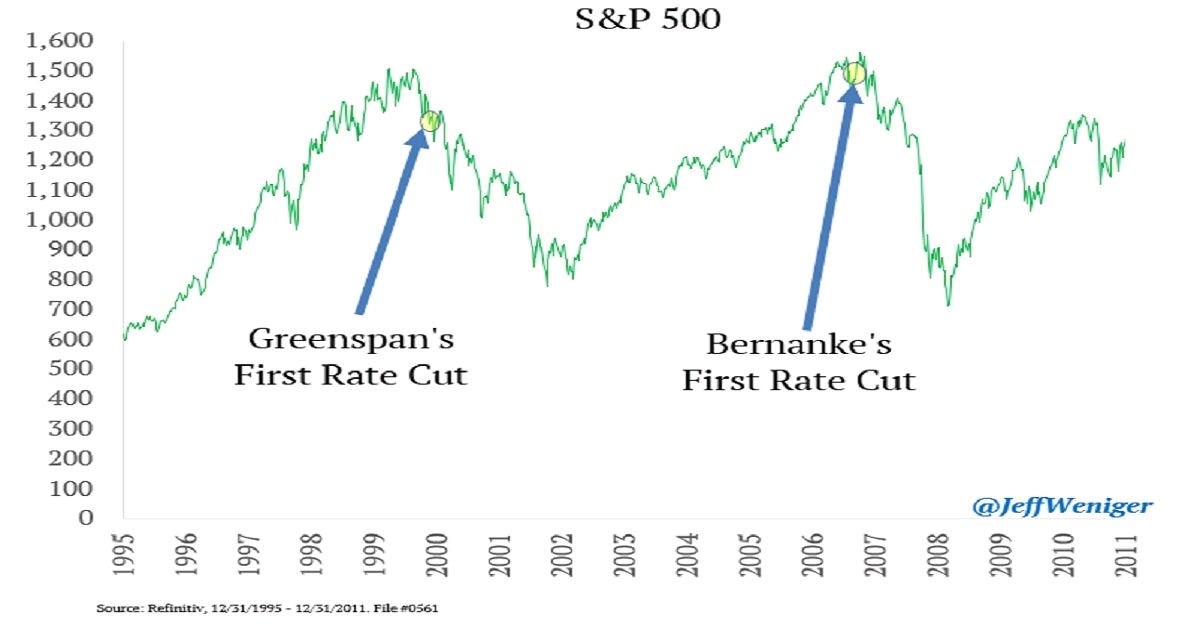

3: It’s not rising rates you need to worry about. Rising rates usually coincide with positive market direction. It’s the delayed effects of these rising rates that cause problems. The effects of those rising rates don’t transmit instantly through the real economy, sometimes taking up to 18 months (more art than science). Of course, by the time this happens central banks are behind the curve and start dropping rates as the economic and market picture deteriorates. Economic indicators are suggesting this point is approaching.

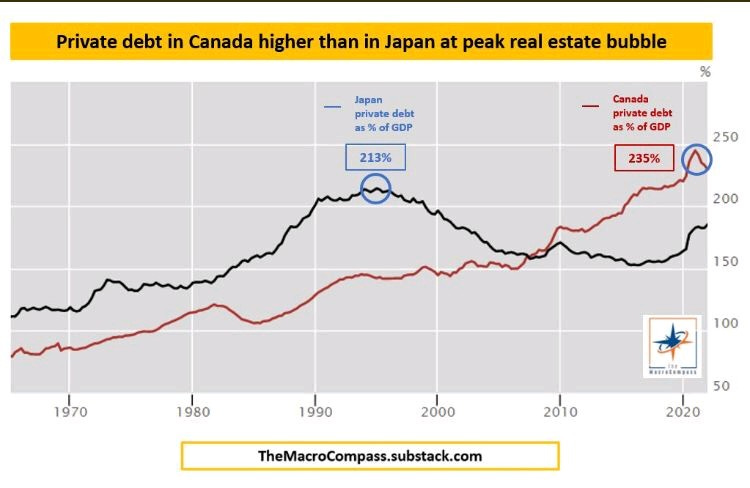

4: Private debt relative to GDP in Canada exceeds the peak of the Japan bubble! Canadians are already under pressure, as declining home prices erodes the net wealth of the most over-extended consumers.

5: The EU is highly dependent on imported oil for its energy supplies, much of which is supplied by Russia.

This is a major strategic point of leverage for Russia. Consider the implications of an energy shortfall in Europe this winter. It doesn’t take much to imagine a scenario that triggers riots and looting.

6: What happens to the renewables revolution when the prices of components skyrockets? Lithium prices have quintupled over the past couple years, and demand is expected to grow. Experts suggest there simply isn’t enough easily accessible raw materials to supply a transition to renewables.