Five chart fun

Assortment of economic and market charts to spice up your life

1: I found this chart to be a bit of a shocker. OPEC spare capacity is getting tighter, but is still more than double the rate for most of the 2000s commodities bull market. OPEC has more spare capacity, as a percent of total capacity, than leading into the Covid crisis. Unless total OPEC capacity has shrunk, this runs counter to the predominant narrative that oil supply is extremely tight.

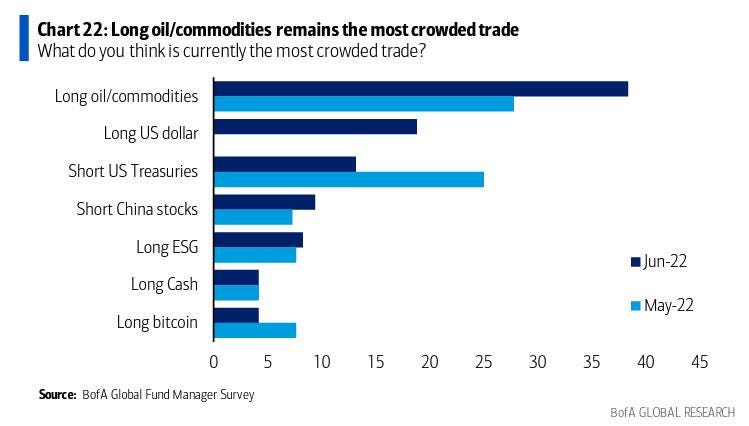

Sort of makes you wonder whether the long oil trade is overplayed (second chart).

2: Despite what seems to be impending economic doom, yield spreads have not tightened by much, if at all. Typically, ahead of recessions (everyone today seems to be predicting recession) yield spreads widen. Today, not so much.

This time might be different because both corporates and sovereigns are selling off to the same extent. Not exactly a positive thing.

3: Currently, the 2s-10s spread is edging near negative territory, as if its getting comfortable with the inevitable. Many analysts are pointing to a recession, however, if history is a guide recession won’t arrive until several months after a clear yield curve inversion.

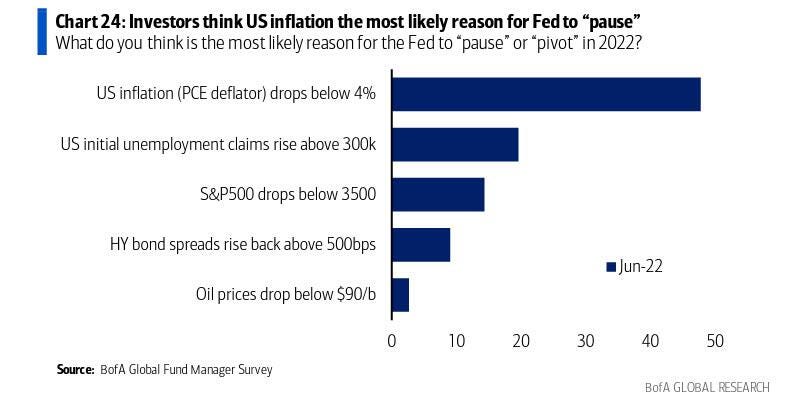

4: Half of investors surveyed don’t expect the Fed to pause tight monetary policy until inflation reaches 4%! Monetary policy takes months (some argue up to 18 months) to impact the real economy (this is called the monetary policy transmission mechanism). This means that by the time inflation reaches 4% (which would take months probably) a half year or more of additional tight monetary conditions is already baked into the real economy. In other words, it’s likely the Fed overshoots and pushes the economy into recession.