Inflation Expectations' Dramatic Shift

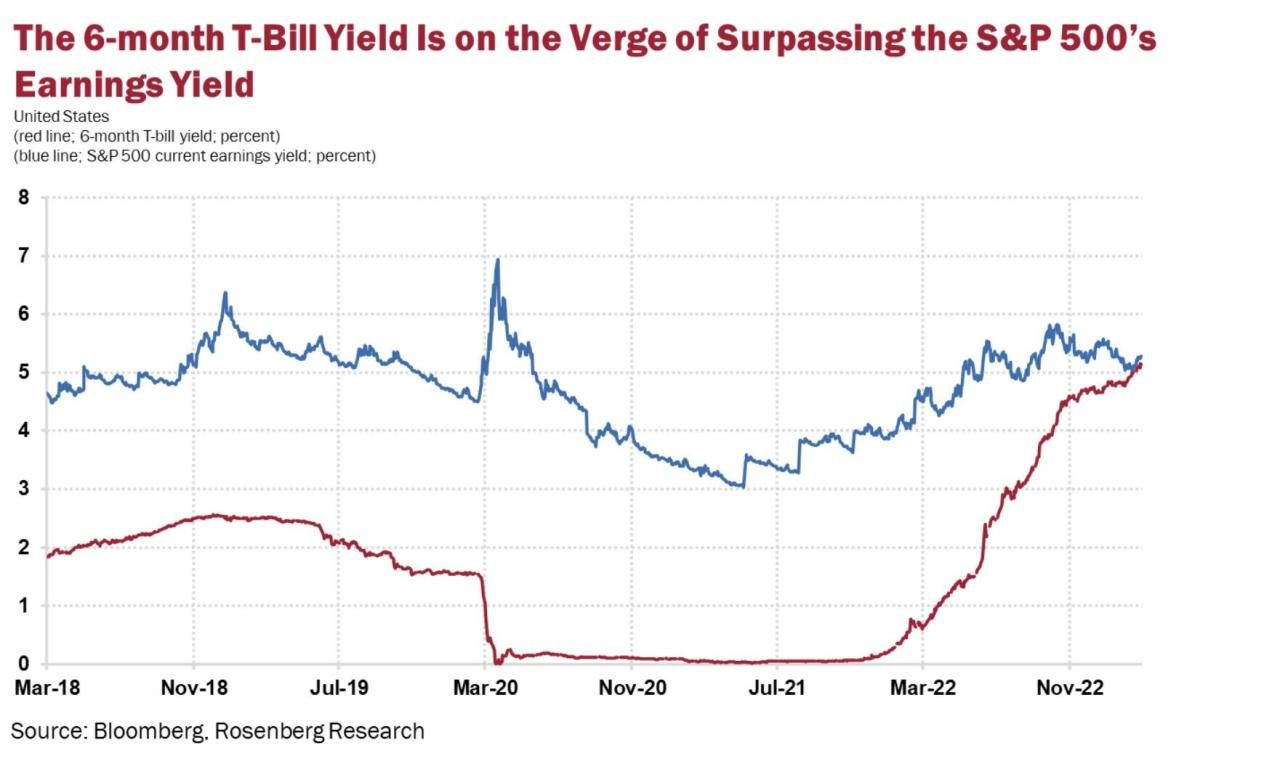

6mth T-bill yields higher than stock earnings yields

Just the facts.

1: Over the past couple weeks the investing narrative has shifted from peak rates and disinflation to a higher terminal Fed Funds rate and higher inflation expectations.

The chart below shows inflation expectations priced into forward inflation swaps. The little spike at the far right represents the recent change in mood.

The second chart below shows Fed Funds rate expectations. There has been a hard re-set since the end of January.

2: Median home prices across the GTA are down anywhere up to 48% year over year! What happens to all those who bought during the pandemic bubble using variable rate mortgages? Word is they’re starting to get squeezed big-time and a significant proportion are in negative amortization (essentially, their mortgage loan principle is increasing with every payment). They’re riding through it by extending the amortization, but that’s essentially kicking the can down the road. Many of these people might be forced to sell at renewal.

3: Inflation. I know this is meant to be funny but inflation is no joke. It is degrading our standard of living. I’m not talking about fancy Caribbean vacations. I’m talking about ordering Chinese food to celebrate your son’s great report card or going on a date with your spouse. After two years cooped up in the house, people were looking forward to living life again. Now we’re allowed to but can’t afford to do anything but watch Netflix.

So why are restaurants still busy? People are going into debt to live their daily lives.

4: Higher short-term rates are creating renewed competition for stocks. The chart below compares the 6mth T-Bill yield to the S&P 500 earnings yield (earnings over price). While this isn’t a perfect comparison - short term vs long term asset, fixed income vs growing earnings, taxes, etc. - it’s symbolic of investor attitudes and the clear indication of the opportunity in fixed income that hasn’t been seen for many years.