Shower thought of the day:

Employees can be fired for “time theft” if they conduct personal activity during work hours. However, many employers expect staff to work during personal time without additional compensation.

Assigned reading:

Cliff Asness: Why Does Private Equity Get to Play Make-Believe With Prices?

Jay Powell’s biggest fear is yet another Fed policy mistake

It’s easy for most people - including myself - to think of today’s inflationary episode as just another hurdle that, once overcome, will be behind us. I think the experience of the Covid-19 pandemic and many other recent crises reinforces this line of thinking. It has been a long time since major developed economies have experienced an acute crisis lasting more than a couple years.

In contrast, the Fed is quietly - yet publicly - concerned about its own mistakes of the past, which, if repeated, could unnecessarily prolong the current crisis far beyond a couple years. In fact, policy makers have thought this way since at least 2002 when Ben Bernanke, during a speech honouring Milton Friedman, blamed the Fed for the Great Depression:

For practical central bankers, among which I now count myself, Friedman and Schwartz's analysis leaves many lessons. What I take from their work is the idea that monetary forces, particularly if unleashed in a destabilizing direction, can be extremely powerful. The best thing that central bankers can do for the world is to avoid such crises by providing the economy with, in Milton Friedman's words, a "stable monetary background"--for example as reflected in low and stable inflation.

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You're right, we did it. We're very sorry. But thanks to you, we won't do it again.

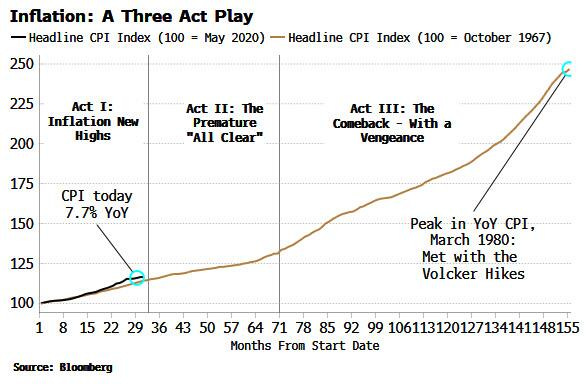

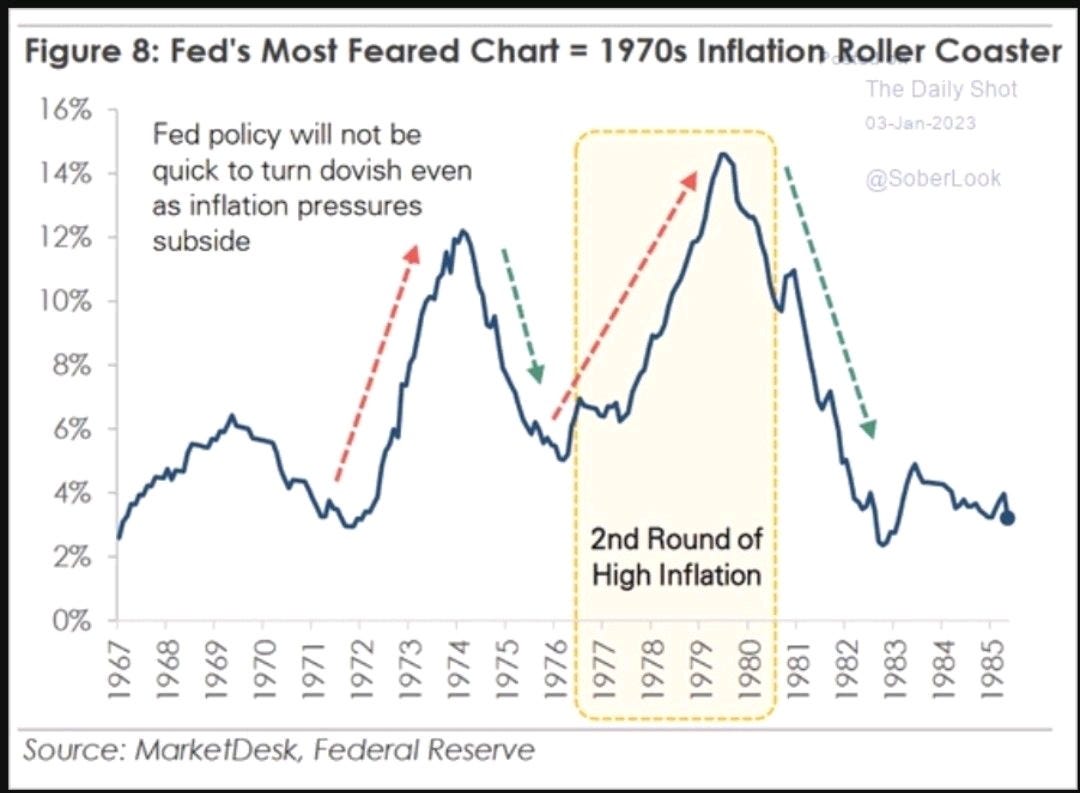

History shows that some of the biggest economic tragedies occured because policy makers were too quick to claim victory. This happened during the Great Depression when policy makers, thinking the recession was over, tightened policy too quickly in 1937. It occured again in the mid-1970s when restrictive monetary policy was reversed at the first signs inflation was easing.

In both cases, the economic crises policy was meant to fix - economic depression and inflation - resurged and became decade-dominating forces.

The charts below show how a premature declaration of victory allowed inflation in the 1970s to come back with a vengeance.

Of course, Fed officials are fully aware of these historical policy errors, explaining why they are often slow to react to changes in data. The mistakes of the 1930s and 1970s are what guide central bankers today. Better to be a Paul Volcker than an Arthur Burns.

For this reason, it is reasonable to expect rates to remain higher until it is abundandtly clear that the inflation demon is dead.