My Macro Notes: Inflation is falling but is that enough?

The next two quarters will illuminate the path for markets and the economy

Inflation continues to fall faster than market consensus

Year-over-year headline CPI hit 3%; core at 4.8%

Month-to-month CPI change around 0.2%, which is at the upper-end of the pre-Covid range

PPI came in below expectations at 0.1% month-over-month

Market still anticipating rate hikes

Despite lower inflation prints, the market is pricing in a high probability of another 25bps hike in the Fed Funds rate to a target range of 5.25%-5.50%

Similar theme across global markets, except for a few outliers (like China)

Market anticipating hawkish Fed because inflation risks remain to the upside

If current month-to-month inflation changes (0.2% for last month) remain constant, future inflation readings could still remain above the Fed’s 2% target

Fed has learned from history and will likely err on the conservative side.

Claiming victory over inflation too soon without clear indication of deteriorating wage gains (requiring a weak labor market) and consistent low inflation reads risks an inflationary resurgence.

A second inflationary surge could require even greater economic pain to get under control.

Why is the market rallying then?

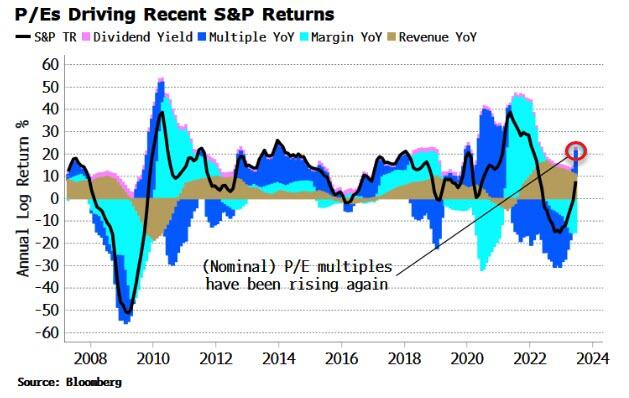

The recent market rally can be fully explained by expanding p/e multiples.

In other words, the rally is not driven by earnings growth. Instead, it is a function of risk appetite and forward expectations.

Many expect earnings to remain flat at best over the next quarter or so.

Without fundamental support, where does the market go from here?

The environment is weakening for both businesses and consumers.

The business climate is weakening (but not dire)

While labor market aggregates appear strong on the surface, anyone actually in the jobs market knows it’s tough out there.

Hiring intentions and private payrolls are both on the decline as businesses anticipate weaker earnings.

Personally, I think the next two earnings seasons will help illuminate the path for both the market and economy.

Consumption is weakening (but not dire)

While the overall US consumer balance sheet remains strong, the average person’s P&L is under pressure.

Excess pandemic savings are gone.

Consumers are increasingly relying on credit cards to fund consumption.