People ask: what should I invest in?

They never like my answer

People sometimes ask me what they should invest in.

They never like my answer.

They want a quick fix: “buy XYZ stock” or “buy ABC cryptocurrency”.

Most people outside of the world of investment finance unfortunately think this is the way to invest. They watch Jim Cramer honk horns and yell “buy, buy, buy!” on CNBC, so they think they’re one great stock pick lottery ticket away from getting rich.

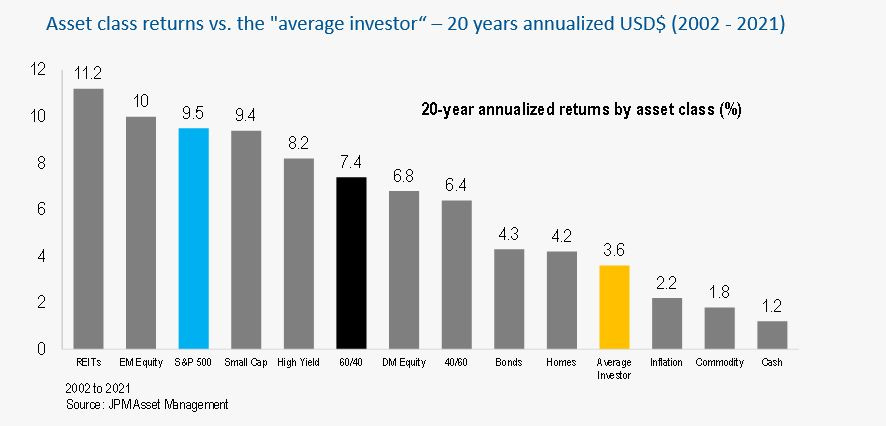

In contrast, the answer I provide is boring as shit and requires effort from the person asking. I know people aren’t interested in my answer because they often drift off as I explain. That’s fine with me, but this is why the average investor dramatically underperforms market returns.

My answers are more philosophical in nature and always start with risk. My answers also involve a lot of questions.

At its essence, investing is about getting the right compensation for taking on a level of risk, and matching that risk to your personal tolerance and goals. I encourage people to contemplate questions like “how much of your hard-earned wealth can you afford to lose?” and “when will you need the money?”.

How do you become a good investor?

To be a good investor, you must become a student of risk. This goes beyond understanding what you’re personally willing and able to tolerate, although that’s a good start.

Most people would be best served by a buy-and-hold portfolio of a diversified basket of low-cost index funds. Choosing the right basket requires one to recognize their own risk tolerance. For many this is where it begins and ends, systematically contributing to the portfolio and accumulating wealth as time proceeds. This has proven to be a good strategy for many people historically.

Still, many investors wish to go further than the buy-and-hold approach and wish to adjust their portfolios over time to take advantage of the market cycle and shifting opportunities. Unfortunately, when people attempt to time the market they can become their own worst enemy.

Estimating where we are in a market cycle requires one to judge the risk aversion of the overall market. There are periods of time when the market is willing to underprice risk, usually during bubbles. In these periods, weak companies IPO, low quality earnings are overlooked, debt covenants weaken and risk premiums shrink. Usually, people fail to recognize the cycle and euphoric market pricing is rationalized one way or another. Sound investment plans morph into feeding frenzies as FOMO takes emotional control, and eventually people - overly confident in their own skills - borrow to obtain what their capital base couldn’t otherwise. Their justification: “why not leverage up if you’re 100% confident you can earn 10% per year in perpetuity?”.

Performance during market bubbles unjustifiably raises the investor’s ego and they start to misread luck as skill. Unfortunately, leverage is often the death knell of the overly-enthusiastic investor when the market moves against him.

Should investors use leverage?

Overexposure via leverage (debt or derivatives) can wipe people out. Leverage amplifies gains and losses, and you can potentially lose all your capital even if the underlying investment doesn’t go to zero. Throughout history, many have been sent to the poor house by levered exposure to a “sure thing”. Remember the saying “safe as houses”? Confidence in that concept almost destroyed the global financial system in 2008.

Many will point to averages and suggest borrowing makes sense as long as the cost of borrowing is below the historical market return of about 10%. Sounds good in theory, but it reminds me of the story about the 6 foot man who drowned crossing a river that was 4 feet deep on average. It turned out the river was 2 feet deep in places and 10 feet deep in others. Averages don’t help when you’re dead or financially wiped out.

Yes, you do want to think long-term to benefit from what the market has historically provided. But you must operate knowing the market will be up 25% in some years and down 35% in others. You must be able to survive those down years if you wish to get anything close to the long-run market return.

The cycle happens over and over, yet people quickly forget. The emotional state amid the delirium of success causes investors to unlearn basic principles. However, the great investors are ones that do learn from history and harness risk cycles to their own advantage.

I’ve included some sage advice from Warren Buffett and John Templeton below.

“Be fearful when others are greedy, and greedy when others are fearful.”

- Warren Buffett

“Bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

- Sir John Templeton

Risk budgeting

In addition to personal risk tolerance and general market mood, investors must also budget their risk allocations properly. Something most investment professionals will tell you is that if you lose, you better make sure you live to fight another day. You must ensure exposure to individual securities, sectors, asset classes and factors won’t ruin you if things go south.

If an individual company goes bankrupt, for instance, you want to ensure your equity position is small enough that you’re not wiped out. Same goes for sectors and asset classes. I think that’s intuitive for most people. However, many overlook factor exposure, such as to interest rates. 2022 has devastated the traditional 60/40 portfolio, as “diversification” broke down. What people missed, however, was that both stocks and bonds are negatively affected by rising interest rates. They weren’t diversified after-all.

Rare risks aren’t so rare

Finally, investors must appreciate that rare risks (aka tail risks or black swans) are not so rare. Don’t discount individual potential low-probability (but high impact) events because they are unlikely to happen. Consider all the “once-in-a-century” events that have occurred over the past couple decades alone. Global financial meltdown, nationwide housing bust, global pandemic, droughts, storms, heat domes. You simply cannot rely on individual event probabilities, because in reality the cumulative probability of something big happening every few years is much higher. Shit is going to hit the fan once in a while. How it affects you and your portfolio may vary, but you must be prepared to accept that something that should never happen is happening and react accordingly - ideally before everyone else.

Takeaway

If you’re new to investing you should learn about yourself and basic investing concepts before even opening an account. Investing is boring and its first principle is to ensure you don’t lose the purchasing power of your hard earned savings.

Be honest about the time and skill you have to invest on your own and consider partnering with a fee-for-service advisor, especially if there’s a chance your decision-making is clouded by emotions.

In my own personal network, people who I'd NEVER think would have the mental or psychological capacity to do the boring work behind investing have bought and sold with the cool comfort of a professional. Anyway, it all ended the way it has always ended. But what really gets me is that the same obviousness that drove their investing when things were going well seems to motivate their anger and incredulity now that things aren't going well. In my own life, I still strive to one day be a successful retail investor. I'm still "up" considerable from when I first started taking it seriously in 2014. But I haven't had time to invest in investing - in large measure due to my own demanding professional career as a professor. This lack of time, however, is a struggle second only to the psychological reactions I have to market volatility and risk - something I haven't yet figured out how to handle. By the way, any books you want to suggest?