Signs point to more weakness

Although this is a bearish post, I’m not fully on the bearish side of the spectrum. There are powerful bullish counter trends in play, such as extreme negative sentiment (contrarian indicator) and declining volatility. Still, if someone put my nuts in a vice, I’d probably say I’m a bear right now.

I’ll change my mind when I see inflation start to decline, as that will mean the Fed can take its foot off the brake. We’ve seen some preliminary signs of a flattening inflationary trajectory (which I’ve talked about previously) but nothing definitive. Perhaps Friday’s CPI print will change that.

Anyway, here are 5 reasons why we may see more market and economic pain in the months to come.

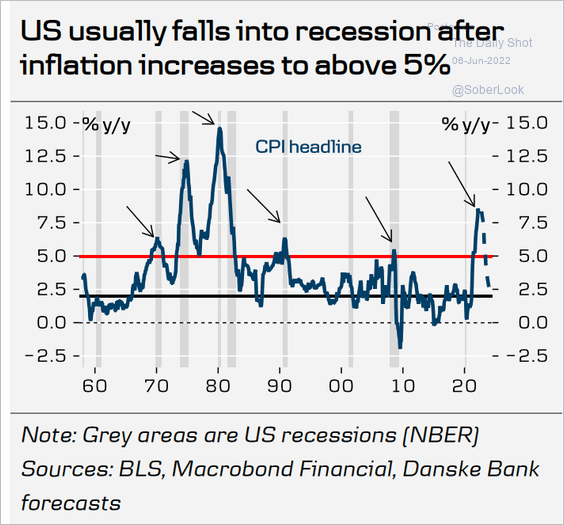

1: High inflation tends to precede recessions, which tend to precede lower inflation. It’s a cycle because high inflation elicits both a demand and monetary (and sometimes fiscal) response.

Inflation increases the cost of living, forcing many to cut back on spending. To tame high inflation central banks tighten financial conditions (second chart), increasing the cost to service debt, thereby suppressing growth.

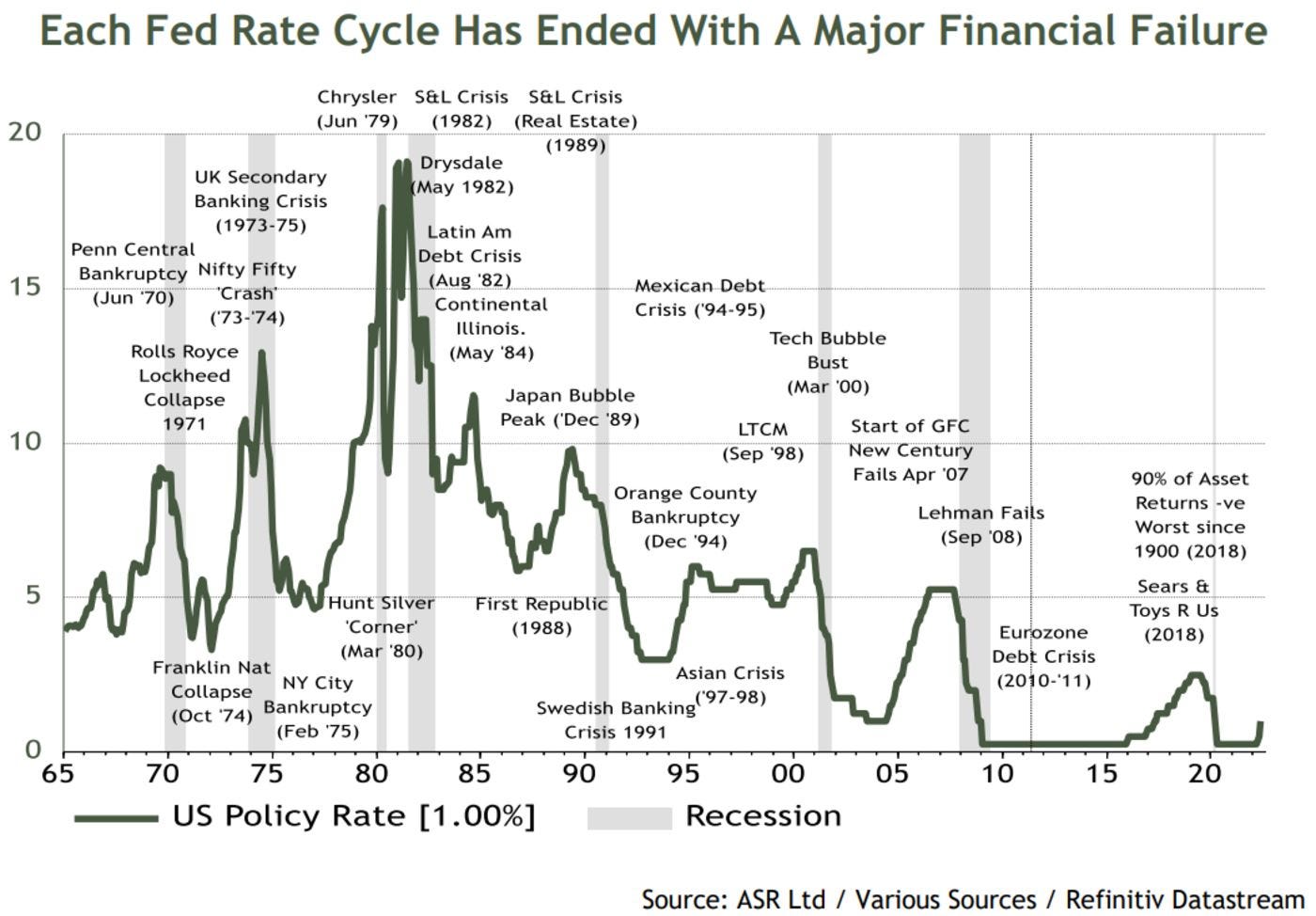

Historically, tightening financial conditions have almost always led to a recession or financial crises.

Note, however, that equity markets tend to bottom before the recession or financial crisis is over.

2: Markets are down, but not that down. If we’re heading to a recession it’s likely markets have more downside, if history is a guide. Although prices have become more reasonable, froth arguably still exists in the market.

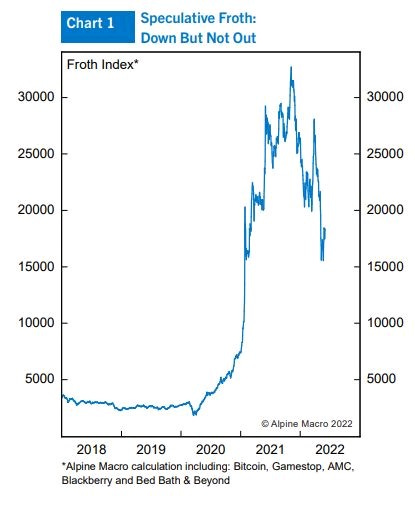

Alpine Macro produced a proprietary (and somewhat rudimentary) measure of speculative froth (below). They argue that the excesses created during the pandemic are far from being resolved.

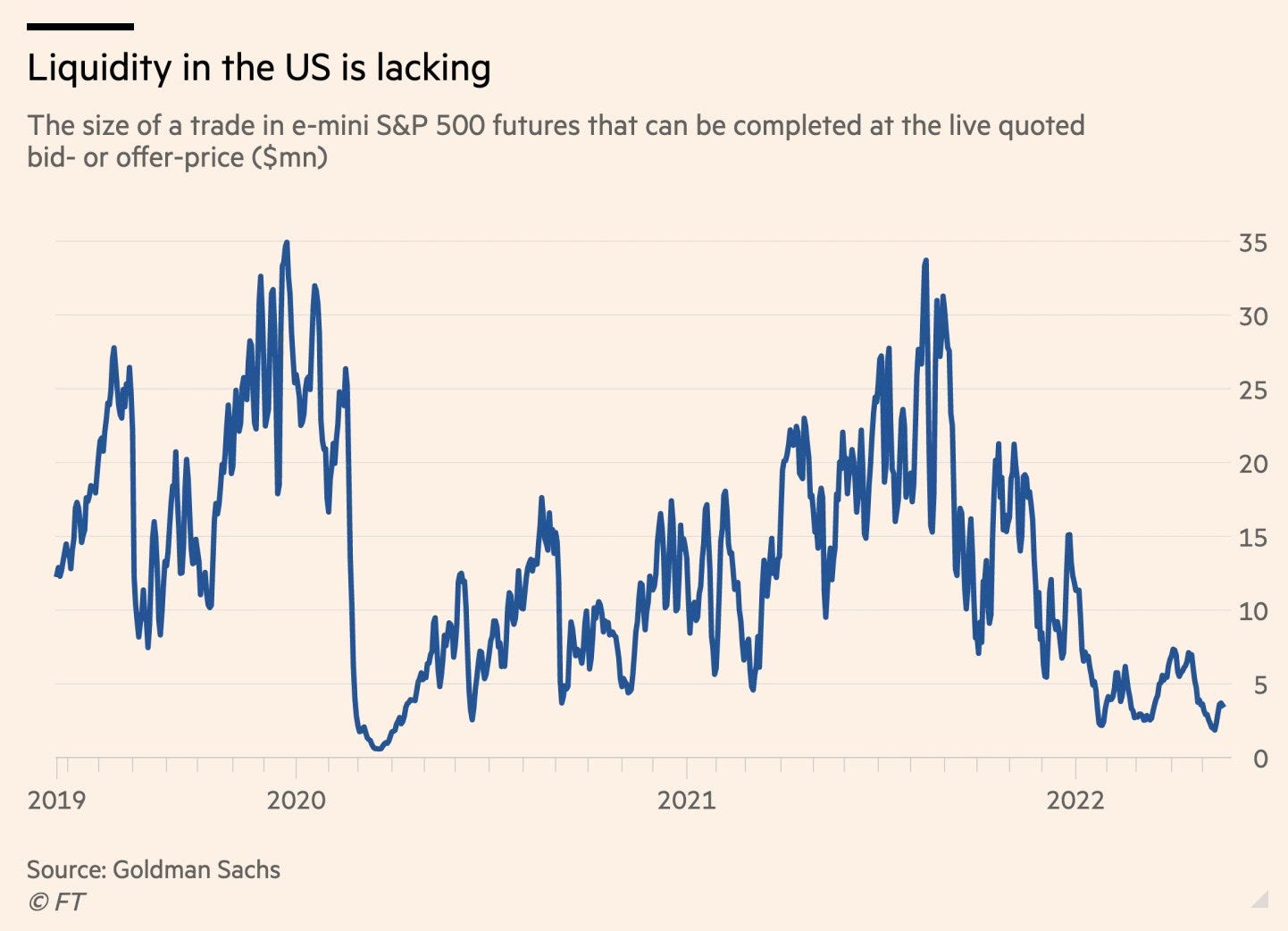

3: Market liquidity is thin. When markets are illiquid, a spark can send investors rushing to the exits at the same time, forcing them to sell at deep discounts to NAV.

4: Businesses are tightening their belts. In response to pandemic shortages, many retailers ordered too much stuff OR ordered the wrong stuff by failing to observe changing consumer tastes. Many retailers also failed to anticipate the impact rising prices could have on demand and profit margins. Excess inventories must now be worked off somehow, either through deep revenue-impacting discounts or by expense-padding write-offs.

Moreover, many businesses - especially those in the tech industry - are starting to slow or even halt hiring. While tech is where most of the froth exists, there are likely to be spillover effects into the broader economy.

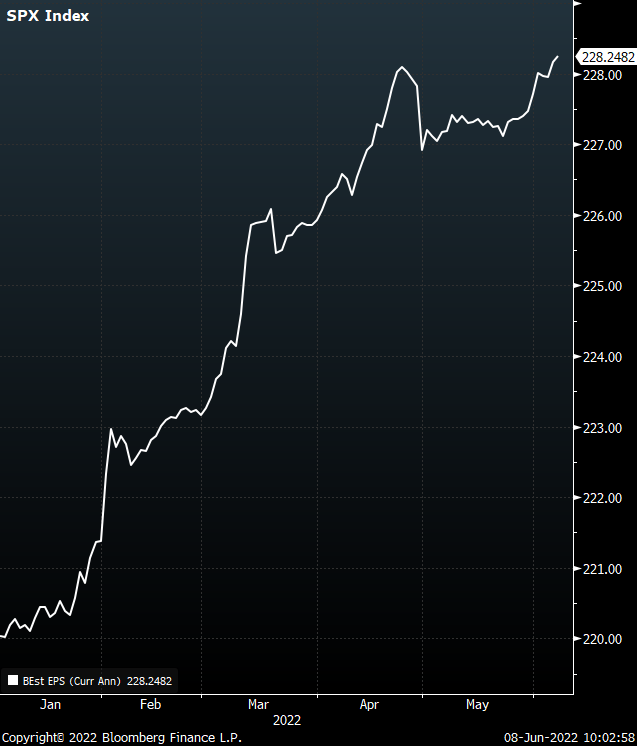

5: Meanwhile, analysts seem to be operating in another dimension, as they keep raising earnings estimates for S&P 500 constituents. Clearly there’s a disconnect. If the analysts are wrong and reported earnings disappoint, share prices are likely to take a hit.