So Where is this Recession?

Also: Big AI Focus at Google's I/O 2023 Conference

1. Post Coronation Party AI Image

The following image was created using Mid Journey - a generative AI used to create images based on prompts. It depicts Prince Harry getting down after his father’s coronation. Although fake, it’s quite realistic and foreshadows a future where we must question everything we see.

2. Google I/O ‘23: All About AI

AI and large language models take center stage

AI is being integrated into all core Google products

This fall: Android phones getting ability to generate customized wallpapers based on prompts and suggestions

Google will partner with Character AI, a startup focusing on building advanced, customizable AI chatbots. The startup is using Google Cloud’s generative AI tools

Google’s A.I. will be used at a Wendy’s drive-through to take orders

Google is bringing generative A.I. directly to Search

A.I. will create entire docs and spreadsheets

A.I. to help write emails inside Gmail

Fun new drinking game: take a shot every time someone in the video below says “AI”

3. So Where is this Damn Recession?

This is the most anticipated recession on record, with forecasts flooding the financial press and blogosphere since early-2022. With equity markets up almost 20% from the October low, you’d think the recession risk is behind us. Could it be possible the recession never materializes?

While equities rally in anticipation of brighter times, the bond market is still predicting a recession in coming quarters. It’s impossible to say who’s right. Instead, let’s look at the data.

Inflation is the primary driver behind macro conditions right now. It is what forced the Fed to dramatically hike rates, causing equities to decline, businesses to pause CAPEX and consumers to hold back on borrowing. Declining inflation will also be what causes the Fed to eventually ease.

Has the Fed Been Successful in its Fight Against Inflation?

While headline CPI has declined significantly, core CPI seems to be stuck around 5.5% - almost triple the Fed’s target. This means the Fed is likely to remain restrictive for some time.

History shows that after a spike, it can take a long time for core inflation to return to target levels. The chart below compares other periods of inflation normalization, and you can see we may only be in the early innings of this fight.

None of this is a secret. Jay Powell continues to clearly articulate his goals, progress and priorities. During last week’s press conference he made the following two statements:

“Inflation remains well above our longer run goal of 2%. Inflation has moderated somewhat since the middle of last year, nonetheless inflation pressures continue to run high and the process of getting inflation back down to 2% has a long way to go.”

“We on the committee have a view that inflation is going to come down not so quickly. It will take some time, and in that world, if that forecast is broadly right, it would not be appropriate to cut rates and we won’t cut rates.”

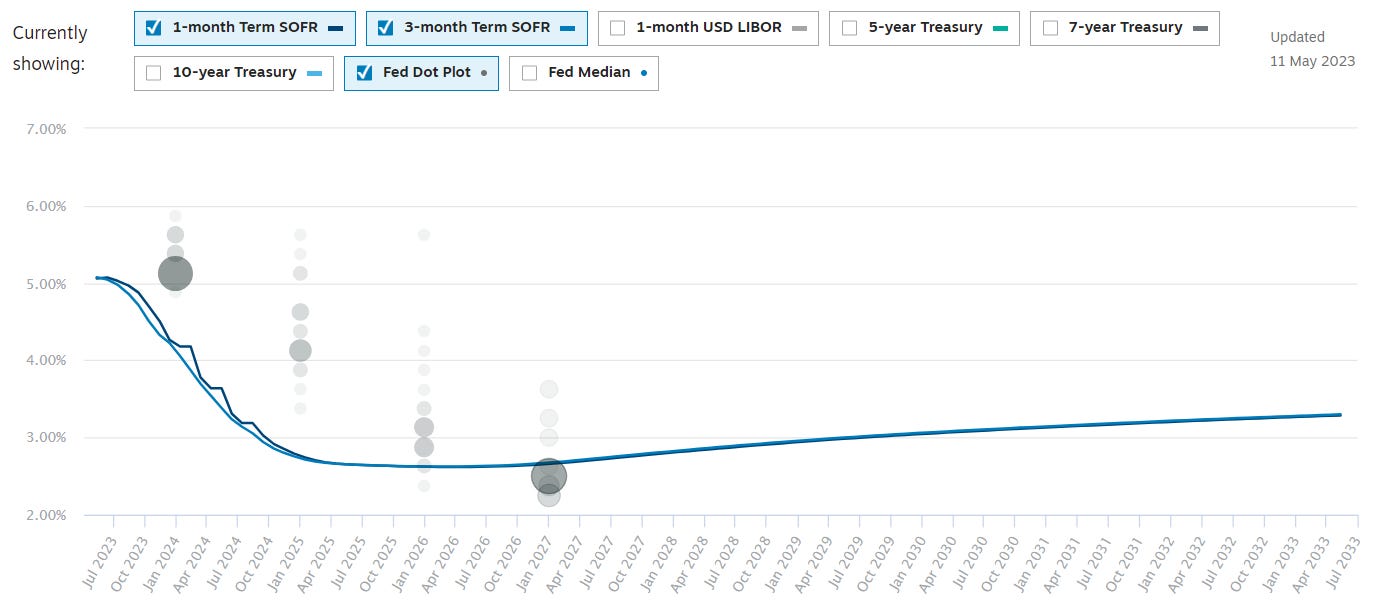

If it’s likely rates will need to remain higher for longer, why is the bond market predicting a decline in rates through 2024? The divergence between Fed policy and bond market expectations might illustrate a potential future breaking point.

Perhaps the Fed succeeds in suppressing core inflation in record time without a hard landing. It’s more likely, however, the bond market is observing today’s Fed policy and believes Powell will remain restrictive until something breaks causing a deflationary spiral, after which he will be forced to pivot. The bond market is expressing what Jay Powell cannot.

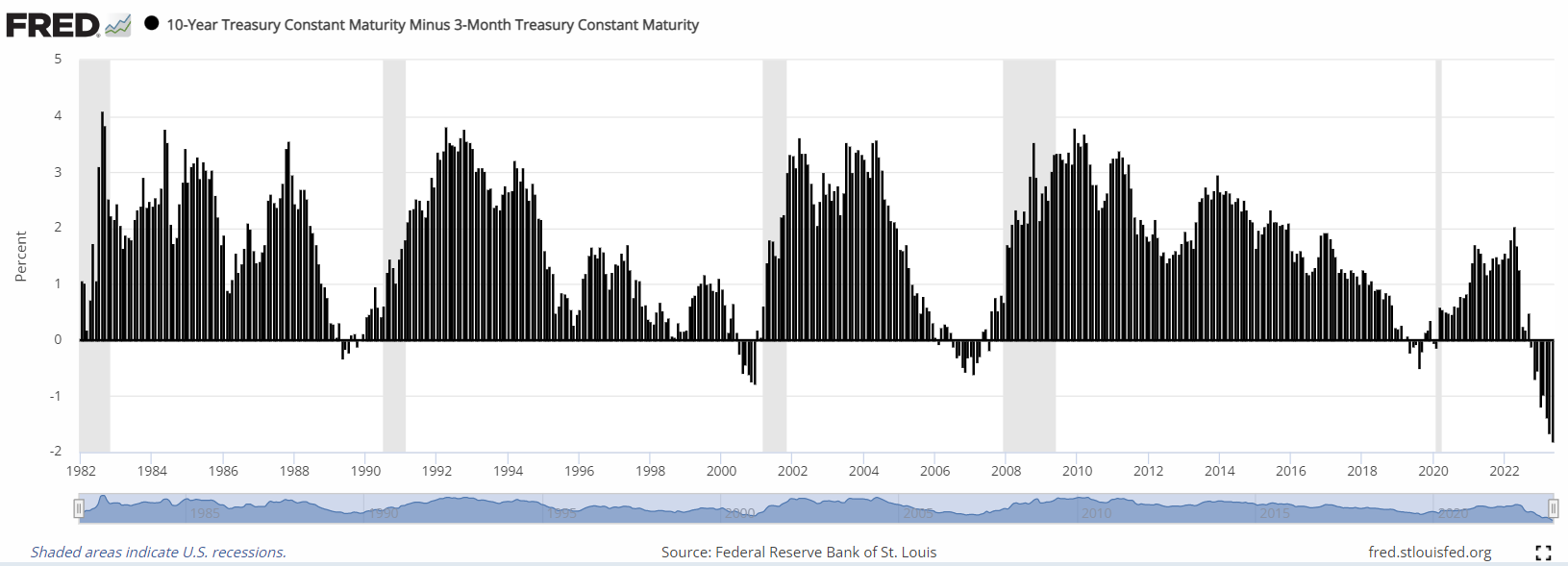

Does the Data Show an Imminent Economic Slowdown?

Other indications continue to suggest an impending slowdown. The 10yr-3mth spread is record-negative. Small business optimism is approaching Covid-lows and heading to GFC territory. Bankruptcies are piling up.

And the cherry on top is the looming debt ceiling debacle, which could drag markets through the mud during the summer. While this is a known issue, markets remain well behaved. This creates a situation where lawmakers believe they have ample political capital to remain unwavering in their position. However, the more unwavering they become, the more likely the issue remains unresolved until the last minute causing market volatility to rise.

Lawmakers might not feel pressure to compromise unless the S&P 500 is down 20% and constituents panic.

Jamie Dimon sums it up: “The closer you get to it, you will have panic”"

By now you’re likely thinking the case for a recession is obvious. The thing is, so does almost everyone else. Every smart investor I meet is either cautious or downright bearish.

So where is the recession everyone has been talking about for months? And will we still be wondering where it is in another 6 months?

The consumer has remained resilient in the face of higher prices and expensive credit. If it turns out that this time is indeed different and everyone is wrong, we could witness a boom in asset prices (as people pile back in) and in economic activity (as companies reinvest in capital and inventories).

While I don’t think this is the base case, I think it’s critical to watch for incremental improvements across a broad range of data points. I am prepared to change my mind with the facts. For now, I am still quite conservative.