The Good, the Bad and the Ugly

Plus: David Rosenberg and Woody Brock go head-to-head on the inflation debate

Popcorn Viewing:

David Rosenberg (Rosenberg Research) and Woody Brock (Strategic Economic Decisions) go head-to-head on the inflation debate

The Good

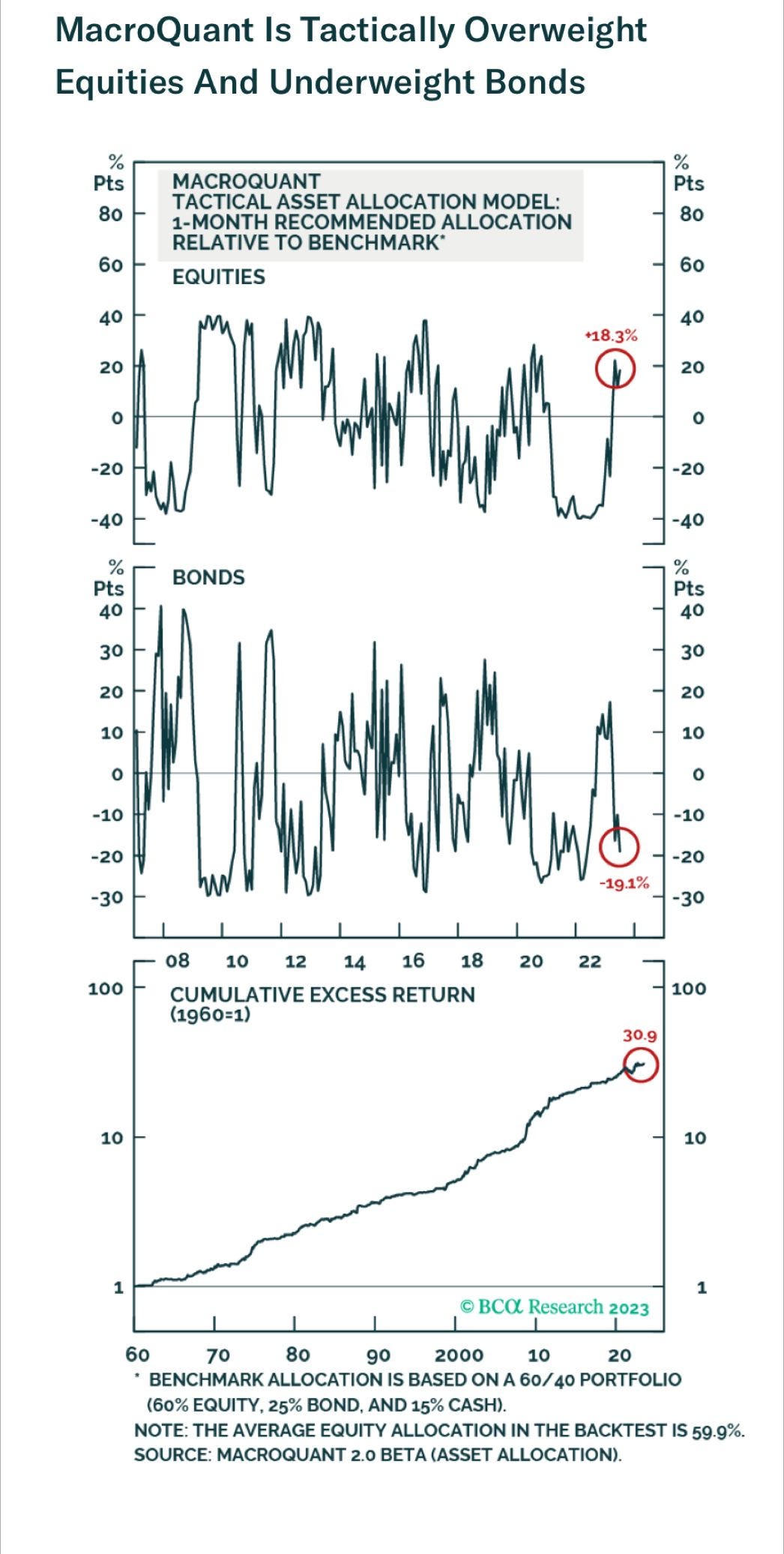

1: BCA Research’s MacroQuant model is making a definitive call to be overweight equities.

2: After major market declines - like the one in 2022 - stocks tend to perform well over the next 1, 3 and 5 years.

The Bad

1: Cash yields are highly competitive with equity earnings yields. While earnings yields and cash yields aren’t exactly the same thing (because earnings grow over time), the convergence of these measures makes the argument for stocks less compelling.

Similarly, the equity risk premium is signaling that stocks are not appropriately compensating investors and is at its lowest point since the dot-com bubble.

2: Mortgage rates remain close to cycle highs at around 7%. While many existing mortgage holders have locked in low rates for 30 years, high mortgage rates should put a damper on US housing demand and labor mobility.

3: LEIs remain in DEEP contraction territory, despite recovering slightly.

The Ugly

1: Weekly bankruptcy filings have already skyrocketed to levels rivaling the Covid-19 collapse and Global Financial Crisis. Strangely, this has occurred with little panic and remains back-page news. This is likely because most of the bankrupt companies are not household names and the dollar value of these bankruptcies is relatively small. The smaller, weaker companies are the first to go. What this tells me is that - despite the high count - we may only be in in the early stages of a credit crisis.

2: What could trigger an a full-blown credit crisis? The debt refinancing wall.

Corporate refinancing risk is slowly growing, as companies will eventually be forced to rollover low-cost debt at higher rates. According to some analysts, many lower-grade companies could see a 50-80% increase in interest expense at the time of refinancing.

Without significant economic stress, rates are likely to remain elevated. However, elevated rates are more likely to create economic stress, causing the Fed to lower rates. It’s a catch 22 that makes a crisis more probable.