The Knot of War

Charts: US dollar reserve status, asset management, rates, TFSAs, carbon neutrality

I’ll start today’s email with a quote.

The following excerpt was taken from a letter Russian leader Nikita Khrushchev sent to President Kennedy when Russia and the US were facing off at the height of the Cuban Missile Crisis.

I wonder if Russian and American leaders are having similar conversations today?

If you did this as the first step towards the unleashing of war, well then, it is evident that nothing else is left to us but to accept this challenge of yours. If, however, you have not lost your self-control and sensibly conceive what this might lead to, then, Mr. President, we and you ought not now to pull on the ends of the rope in which you have tied the knot of war, because the more the two of us pull, the tighter that knot will be tied. And a moment may come when that knot will be tied so tight that even he who tied it will not have the strength to untie it, and then it will be necessary to cut that knot, and what that would mean is not for me to explain to you, because you yourself understand perfectly of what terrible forces our countries dispose.

Consequently, if there is no intention to tighten that knot and thereby to doom the world to the catastrophe of thermonuclear war, then let us not only relax the forces pulling on the ends of the rope, let us take measures to untie that knot.

— Nikita Khrushchev writing to John F Kennedy during the Cuban Missile Crisis

Today’s Charts

1: Asset management company revenues will increasingly be generated by sales of alternative investment products. Why? Because vanilla actively-managed equity and bond funds are easily beat by index trackers, pushing down margins.

In contrast, alternative investment products are more opaque making it more difficult to judge performance against a broad benchmark. When one can’t properly evaluate the value of a product, it’s more difficult to determine the price one should be paying. Consequently, asset managers can pad their fees. Of course, with money moving into alternatives (second chart), the asset management industry will only be more than happy to oblige.

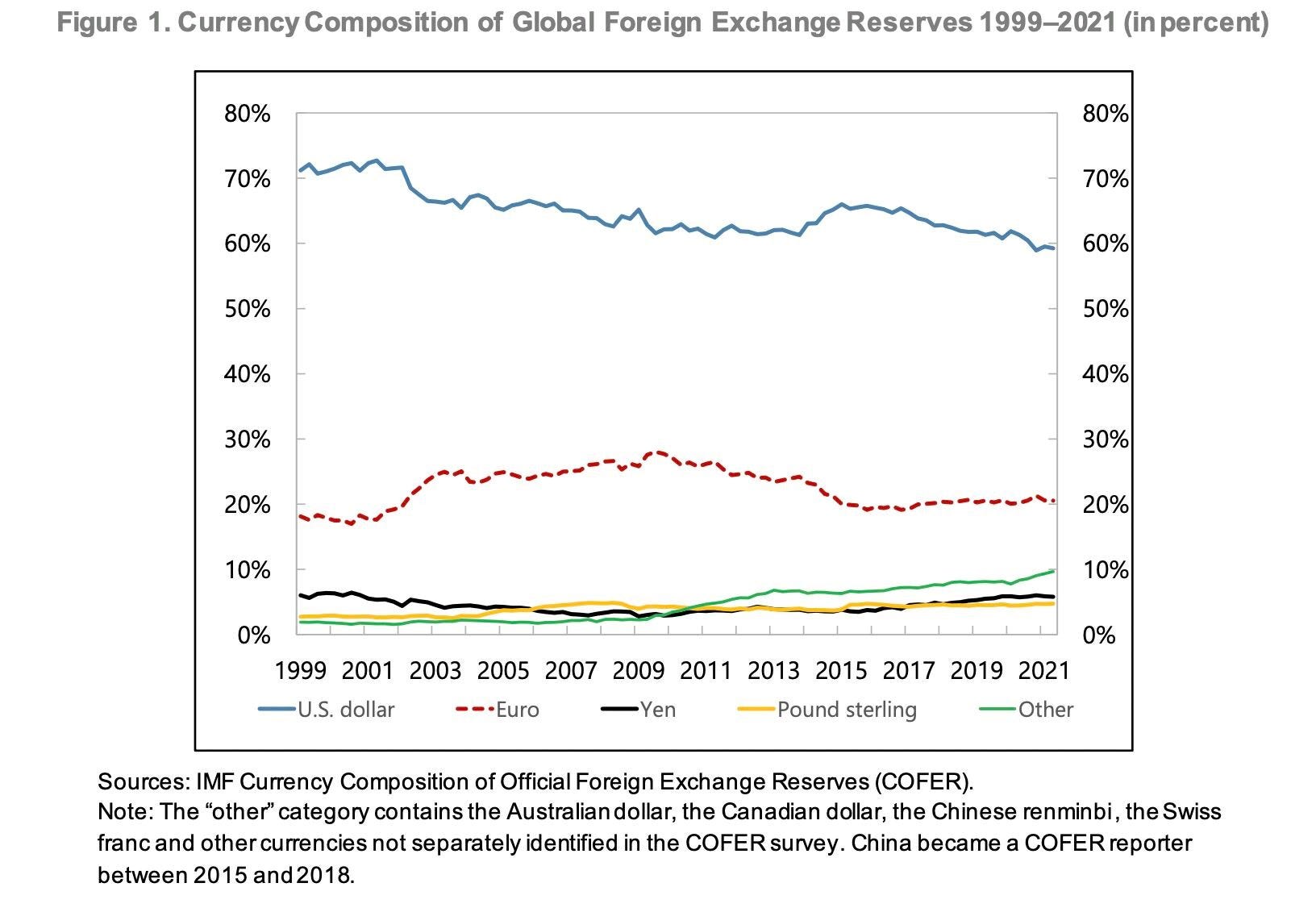

2: While it remains the world’s reserve currency, the US dollar’s importance has been under pressure for two decades. In 1999, the dollar made up over 70% of global FX reserves. Today that number is closer to 60%.

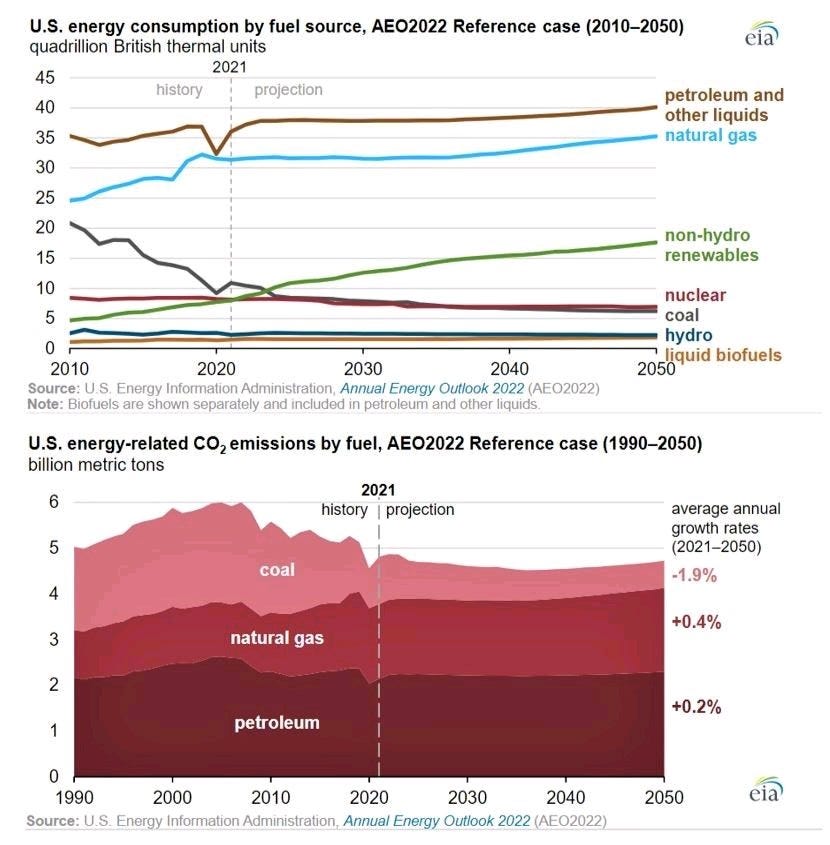

3: Despite the growth of renewables and carbon neutral pledges, US energy consumption derived from petroleum and natural gas is expected to rise between now and 2050. Likewise, fossil fuel emissions (second chart) are predicted to remain constant. So how does the US get to ‘carbon neutral’? All signs suggest carbon neutrality plans rely on unproven carbon extraction and sequestration technology.

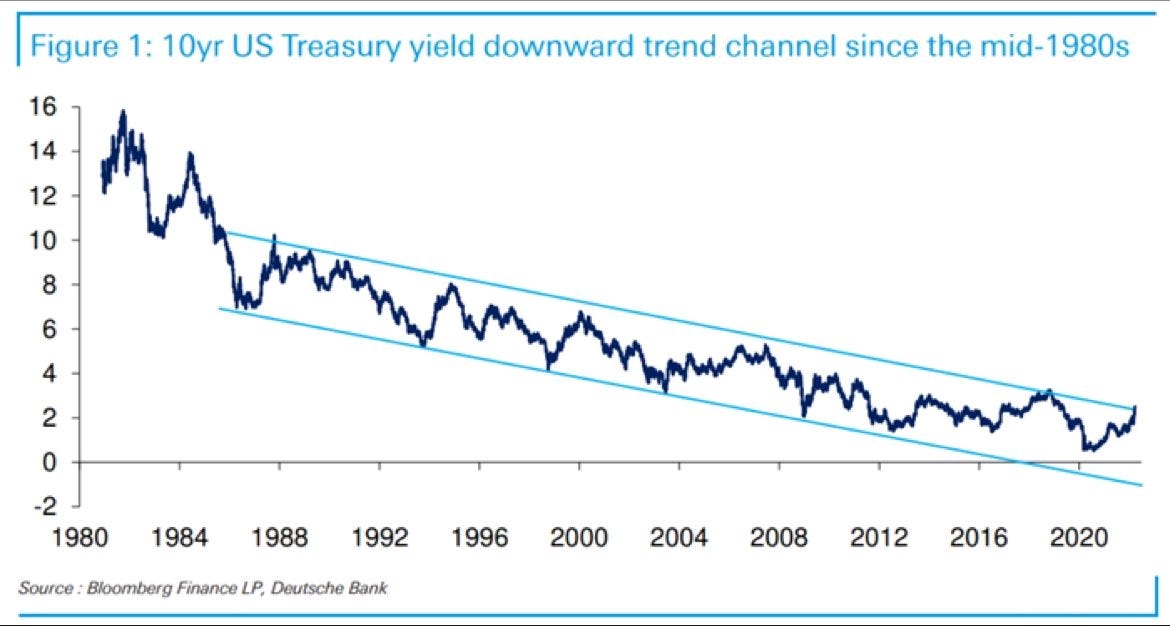

4: The 40 year downward channel for 10 Year US Treasury Yields has been broken. Obviously, yields can’t go down forever. It is therefore reasonable to expect the pattern of long-term rate movements to either flatline or rise going forward.

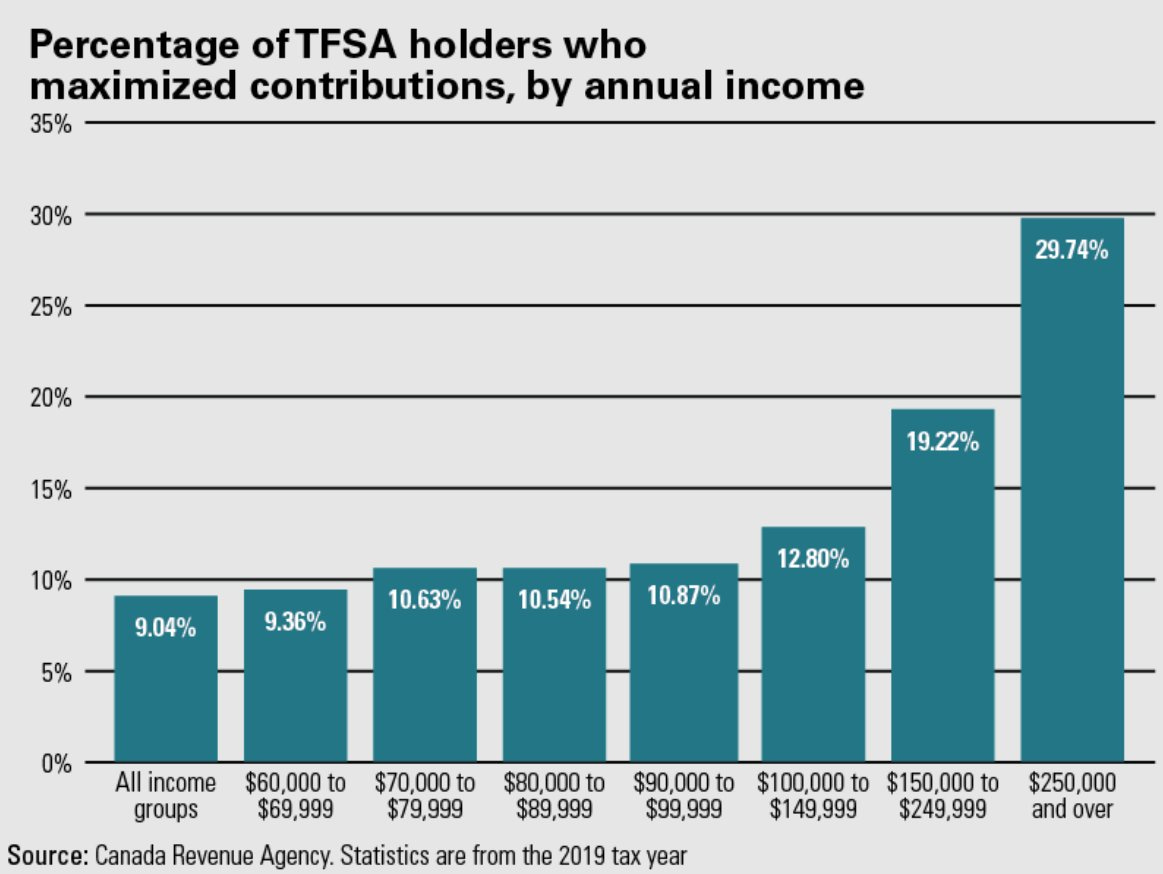

5: Very few Canadians are maximizing contributions to Tax Free Savings Accounts (TFSAs). Despite the word ‘savings’ in the name, these are investment accounts that allow money to grow tax free. Even the highest income earners - those that would presumably benefit most from tax elimination - aren’t maximizing contributions. Could this be an awareness issue? Lack of discipline? Bad planning

Financial advisors take note.