The R Word

Yield curve, market internals, deflationary shocks

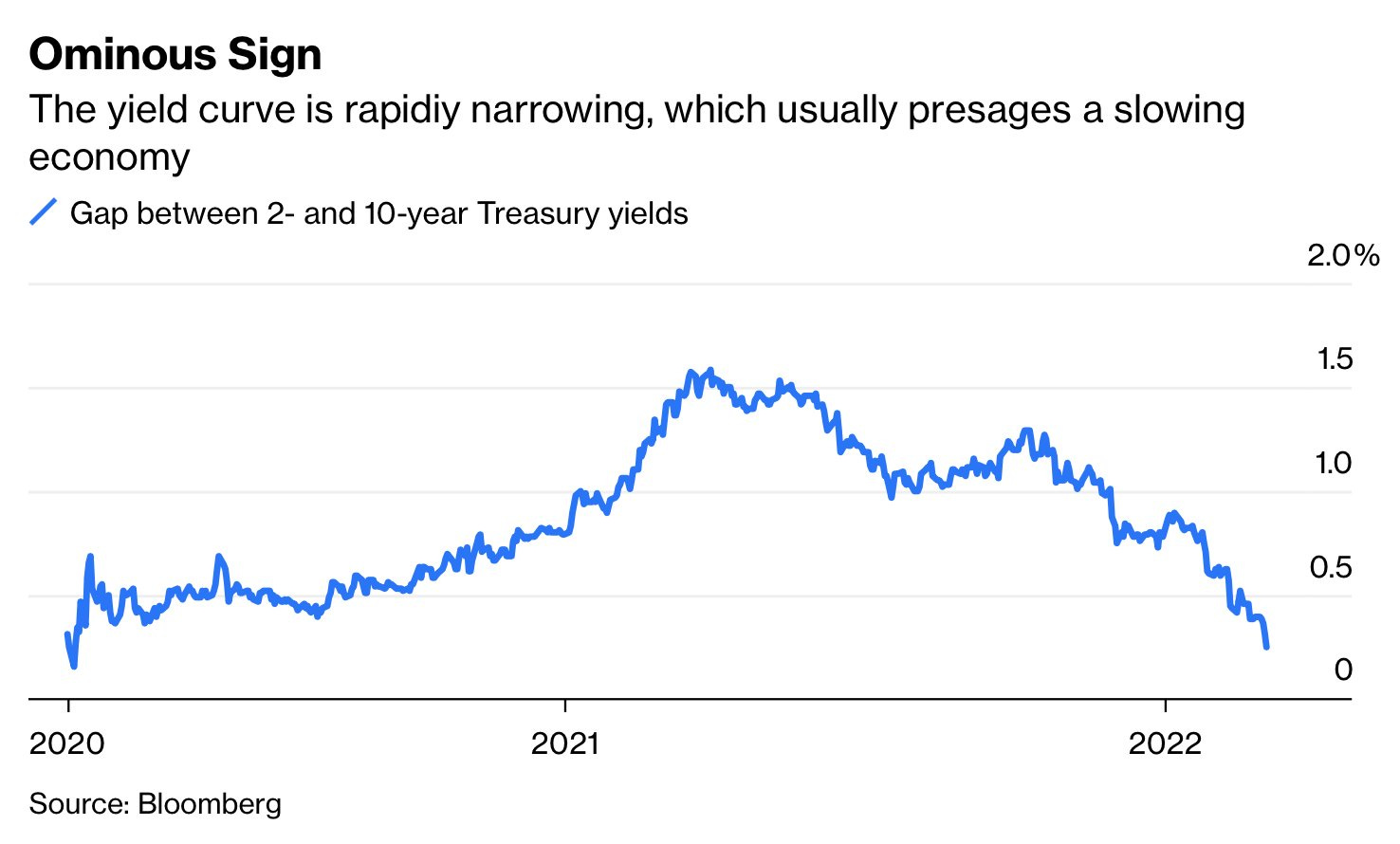

1: The spread between 2yr and 10yr US Treasury bonds is rapidly tightening. In other words, the yield curve is flattening. Yield curves tend to flatten - or invert - when the bond market anticipates a recession. At the very least, this suggests the market is experiencing a growth scare.

The opposing view argues a recession is unlikely because corporate earnings are at record highs and employment is very strong. The problem is both metrics are backward-looking. Today’s reported earnings are based on activity during the past quarter or year. And the business case for today’s hiring is built off that historical corporate strength.

At the very least, I expect more chatter about slowing growth. And this could negatively impact market returns (which are already down about 10%).

2: Although the broad indices are only down about 10% from their highs, market internals are very weak. The proportion of S&P 500 stocks trading above their 200 day moving average is shrinking. Many stocks are down multiples of the broad market, indicating a handful of big names are holding things together. This doesn’t necessarily imply the market goes up or down, but these are not the characteristics of a healthy market.

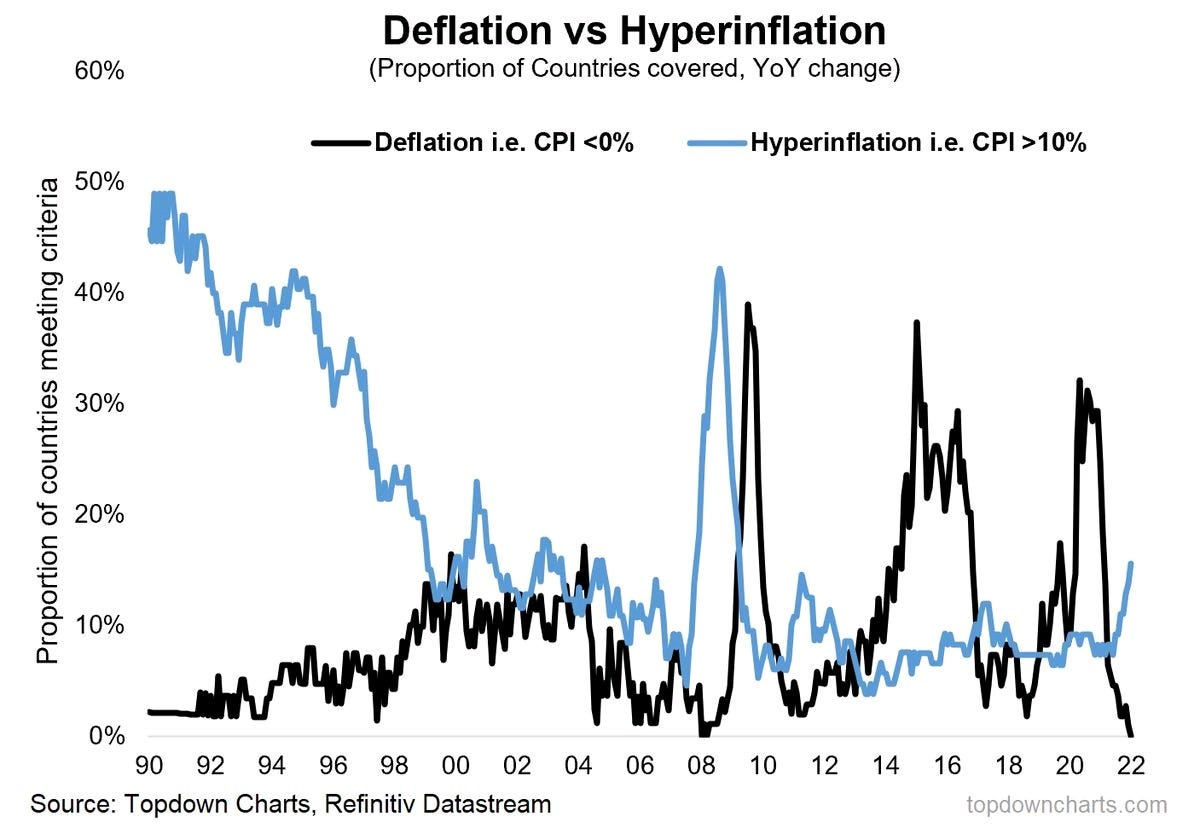

3: Deflation is dead…for now. The chart below shows the proportion of countries experiencing deflation vs those experiencing significant inflation. Currently, inflation is winning.

Note that since 2008 the world has experienced repeated big deflationary shocks as multiple crises tore through the global economy. Could we see this again? Like in 2008, high inflation could eventually cut into spending enough to expose the fundamental fragility of the economy and financial system, resulting in another deflationary shock.

Of course, today’s wildcard is war. War (and pandemics) tend to be inflationary.