Today's market charts

Today's market charts

Stretched valuations, portfolio bond allocations and 1970s performance

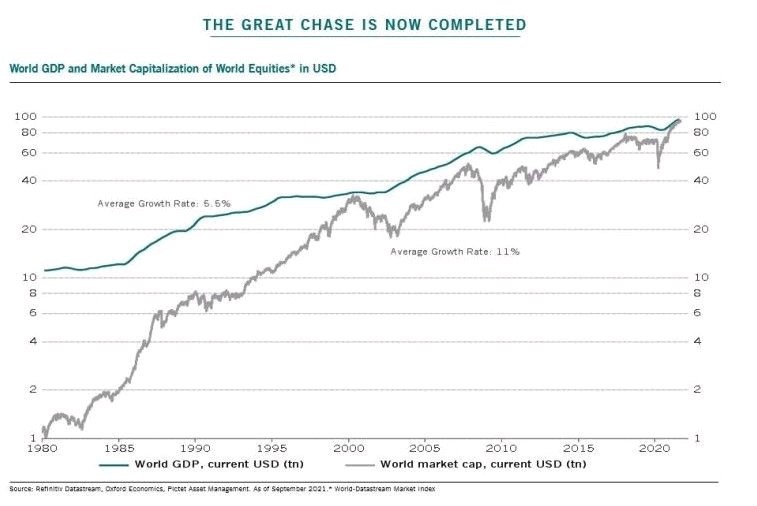

Fact 1: Valuations are stretched. Global market capitalization of all companies has just exceeded world GDP for the first time. And cash flow as a proportion of market cap is at a new low. The million dollar question is this: given current yields and liquidity, are valuations justified?

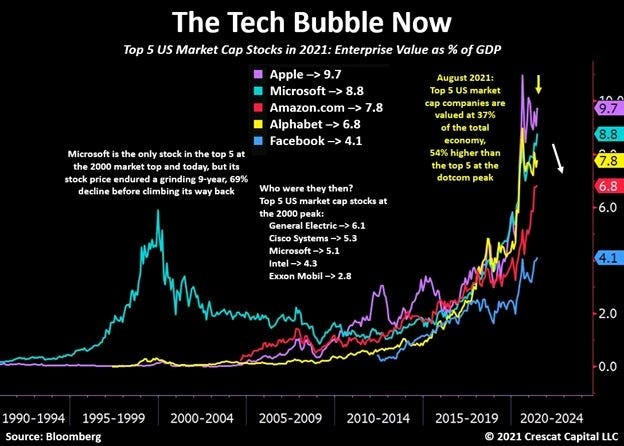

Fact 2: The 5 largest US companies today are valued at 37% of GDP. This is 54% higher than the 5 largest companies at the peak of the dot com bubble in 2000.

Fact 3: The market hates bonds right now. Understandably so, as real yields (nominal yields less inflation) are negative for most fixed income securities. Allocation to bonds has hit a 17 year low. Of course, some would point to this as a possible contrarian indicator.

Fact 4: Some argue that we are in a stagflationary economic environment, reminiscent of the 1970s. During the 1970s, gold was the top performing asset class.