Wednesday Morning Charts

Was October the bottom?

The market is playing chicken with the economic data. Risk-on has outperformed handily year to date, with many of the worst performers of 2022 rocketing higher.

Did the October low mark the bottom? Maybe, maybe not. It would be a remarkable achievement if the Fed managed to engineer a soft landing while tackling aggressive inflation. Anything is possible, and inflation certainly is winding down - possibly to the low-mid single-digits by year end.

At the same time, China is on a path to reopening and, despite numerous ugly economic data, the IMF is revising global and US growth forecasts upward. The IMF still predicts 2023 will be slower than 2022, but their revision upward potentially marks an inflection point for forecasts.

This doesn’t mean I’m diving head first into risk assets. As I’ve said many times, I’m a conservative investor. I don’t like to lose money. My assets represents the sum total of my life’s work and I don’t want to toil any longer than I have to. It is much easier (and faster) to lose money than to make money, so I don’t let FOMO persuade me to take excessive risks. Of course, one must take on some risk to maintain real wealth over time. Ultimately, investing and wealth management is a balancing act between missed opportunities and regret. Luckily, relatively safe assets now provide interesting yields.

Forecasters attempt to see the landscape before the fog clears, and mistakes are part of the game. The key to success and longevity is to prepare for these inevitable mistakes. Data is emerging to help investors see the full picture, but since it is a discounting mechanism the market will look through this data to the future.

Stay tuned on Wednesday for more data (ISM Manufacturing PMI, JOLTS Job Openings, Fed rate decision and presser) that might confirm which way we’re headed.

While you hold your breath, here are a few charts to help explain the state of the markets:

1: Due to much a much higher household debt to GDP ratio in Canada vs the US, the Bank of Canada will likely need to act more delicately than the Federal Reserve.

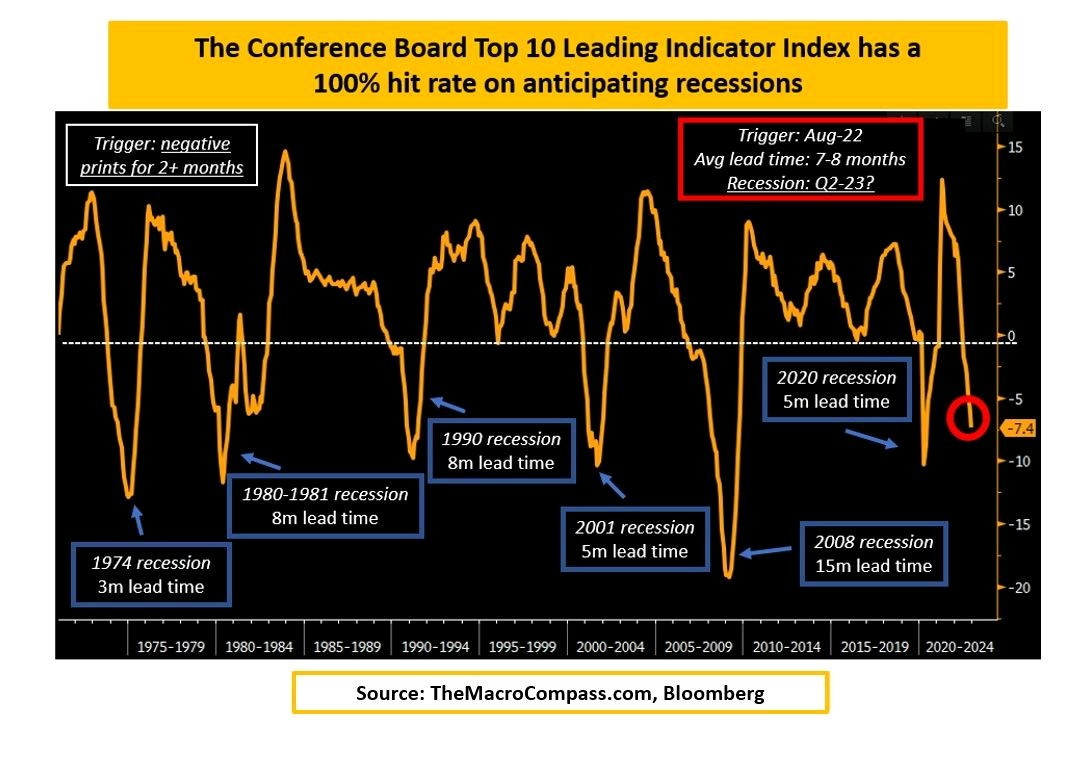

2: Leading economic indicators suggest the widely anticipated recession will begin around Q2 2023.

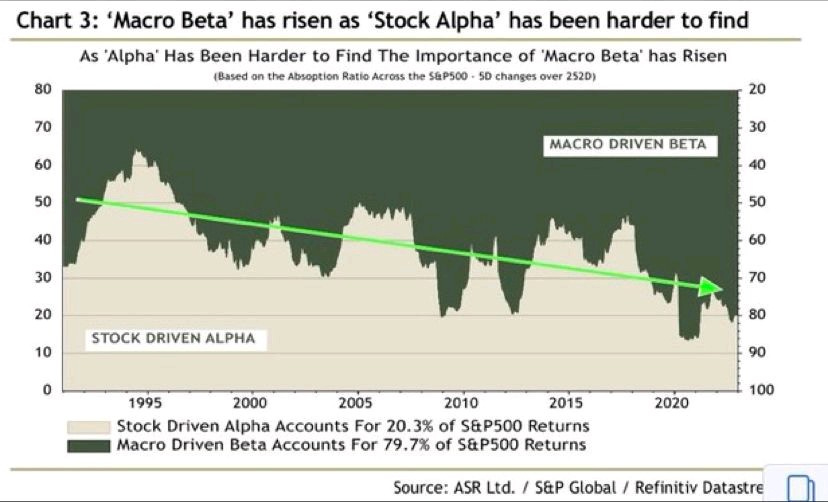

3: This chart breaks down sources of return for the S&P 500 into two components: Beta and Alpha. Beta is the portion of returns that can be explained by broad market movements (macro), whereas Alpha is the portion of returns explained by stock-specific performance.

Increasingly, Beta has become the dominating force, explaining 80% of S&P 500 returns. It appears, therefore, that it is increasingly important to pay attention to the macro environment.

4: Low interest and ebullient investors prop up poorly run companies. As the tide goes out, naked business models get exposed. Currently, almost half of Russell 2000 constituents are unprofitable. Higher interest rates and low investor risk appetite could push many of these companies into the abyss.

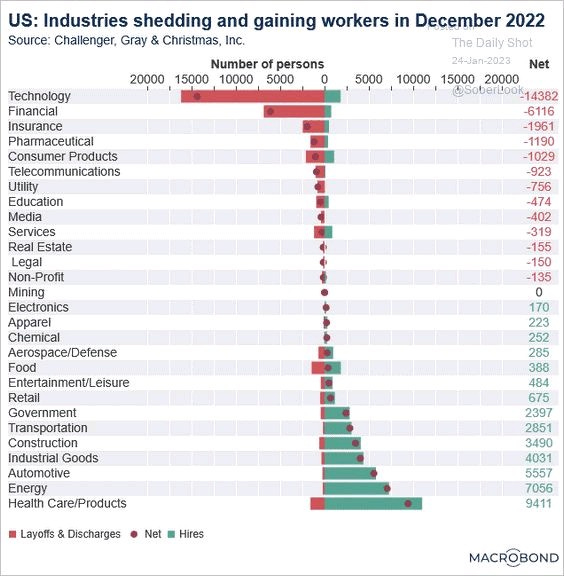

5: So far, layoffs have been concentrated in Tech and Finance sectors.