When the Rich Feel Poor

Americans ill prepared for a future they fear

Psychology is a huge part of long-term wealth creation.

How investors manage their emotions and behaviors determines their ability to save and grow their assets.

Behavior is often determined by one’s experience and view of their standing in the world. For example, someone who grew up in a poor household is likely to retain thrifty behaviors throughout their life regardless of their wealth.

Often, attitudes towards money conflict with the hard data so it’s important to question assumptions and bridge the gap between perception and reality. Compound this with the number of heuristics programmed into our lizard brain and it’s a recipe for Akrasia.

Below are a few examples:

Disconnect between Priorities and Actions

61% of Americans say they are more afraid of running out of money than they are of death. (Source)

Yet many aren't preparing for the future.

⚠ 40% say they don’t have a financial plan for retirement and will just figure it out when they get there

⚠ 56% don’t know where to start planning beyond having a basic retirement account like a 401(k) or IRA

⚠ Only 42% have a written financial plan

Why the disconnect?

People often prioritize the immediate over the future, especially when planning for the future can take away from the ability to satisfy current needs.

Instant gratification is endemic because most people lack the discipline to plant seeds for tomorrow. To be fair, many people also lack the means to prepare.

So they approach their twilight years without a plan, simply hoping for the best.

When Expectations Meet Reality

Conversations about retirement often center around a dollar figure. Often that dollar figure is so high it feels out of reach for most.

Do investors truly require a $1 million nest egg to comfortably retire? Perhaps, but despite concerns over running out of money about half of American families aren’t saving at all.

According to the Wall Street Journal, half of Americans have nothing saved for retirement. Only 3.2% are in the coveted million dollar club.

Between the two extremes exist a desert of savings. It is clear that few are on track to hit target retirement goals.

Investors need help connecting audacious expectations (“I need $1MM to retire”) with the reality of consistent, manageable, achievable actions (e.g. a regular investment plan).

When the Rich Feel Poor

While many Americans aren’t saving at all, there’s a segment of society that is successfully building wealth yet feel they aren’t achieving their goals.

It is possible this disconnect is what drives them to build wealth in the first place. However, there comes a time in life when one has to take stock and celebrate their achievements.

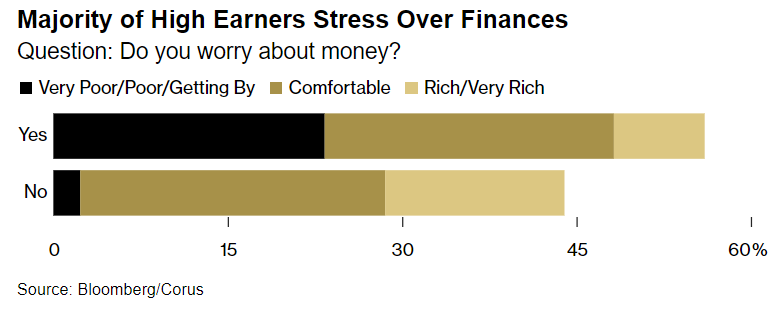

A recent survey looked at why the rich - defined as making at least $175,000 a year - feel poor. It found that 25% of wealthy Americans consider themselves "very poor", "poor" or "getting by...".

Same goes for Americans with significant net worth (chart below).

Why does a big portion of the wealthy feel poor?

Answer: “Wealth” is subjective, relative and a moving target, and biases and experiences shape patterns of behaviors.

(Source)

Here’s what people say when asked if they’re “rich”:

“I still worry about money,” said Debra Corbin, a 67-year-old retiree in Naples, Florida, with a home worth more than $1.3 million. “I think rich is subjective. When I’m in southern Illinois where we're from I feel rich. When I’m in Naples, I feel blessed. Down here it’s hard to feel rich because there are billionaires down here.”

“I grew up quite poor, and I know money can be taken away,” said James Bramble, a 53-year-old attorney in Salt Lake City who makes about $350,000 a year. “To really feel rich that I think you would no longer have to depend on money — like if you didn’t work, you’d still be okay for the rest of your life, and I’m not there.”

“To feel rich, I would have to own my house free and clear without mortgage, pay for my kid through college and have more liquid cash in the bank,” said Erika Wilson, 45, who has a household income in the “low six figures” and lives in Durham, North Carolina. “I worry about future expenses and increasing inflation.”