When the tides turn

What happens when inflation starts coming down?

There will come a point - perhaps over the next few weeks or months - at which there will be more clarity on the direction of inflation, interest rates and economic growth.

If, as many expect, 10 year Treasury yields are close to peak and the economy begins to slow, some of the trends we’ve experienced year-to-date could shift.

What’s worked YTD:

Value

Energy

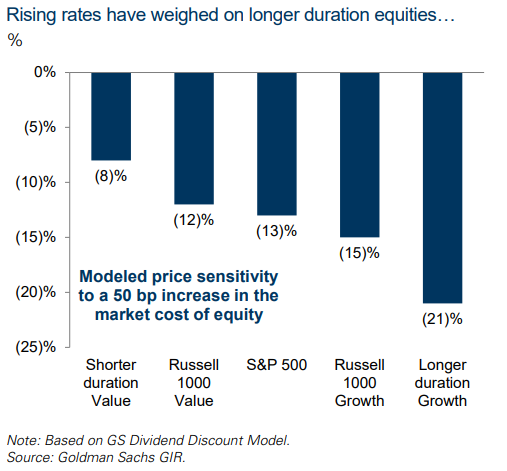

Short duration assets (relative to long duration assets)

What hasn’t worked YTD:

Growth

Tech

Long bonds

The YTD experience (underperformance of long duration assets) is what you’d expect in an inflationary environment chased by rising yields (and rising real yields).

Rising yields means money is more expensive, pushing up the discount rate by which future cash flows are valued. The farther into the future the cash flow, the lower the present value. Relative to value companies, high growth companies are most vulnerable to rising rates because a huge portion of their valuation is dependent on a larger weight of cash flows far into the future. Generally, high growth stocks are higher duration assets than value stocks.

If economic growth begins to slow, inflation moderates and yields decline I would expect something quite different from the YTD experience. Namely, if the tide turns high duration assets - growth stocks (like those in the tech sector) and long term Treasuries - could outperform.

The question is this: What does the journey from here to there look like?

I don’t know when the tide turns. Perhaps tech and long-dated Treasuries continue to underperform for a while. But the bear market has already removed much of the froth from both asset classes. Big cap tech valuations (chart below) are trading at valuations not seen since December 2008, so they’re worth a second look.

I’m not saying prices can’t fall further. This depends on the depth of the looming economic slowdown and the degree to which inflation and yields moderate.

A shallow slowdown coupled with tamer inflation and softening yields could benefit both tech and long duration Treasuries. A deep recession would likely only benefit long duration Treasuries and potentially send stocks down another 10-20%.

As I regularly remind readers, I’m not a soothsayer. I am just an analyst trying to make sense of a puzzle where the pieces are constantly changing shape and colour. Regardless, as the days pass, I am becoming more interested in long duration assets.

My view will sharpen as I get a better visual on inflation, yields and economic growth.