Will the Fed continue to fight inflation?

Getting ahead of Wednesday's 1pm Fed announcement

“Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man.”

Ronald Reagan

Inflation has only just started to moderate and Fed Chair Jay Powell’s job isn’t done.

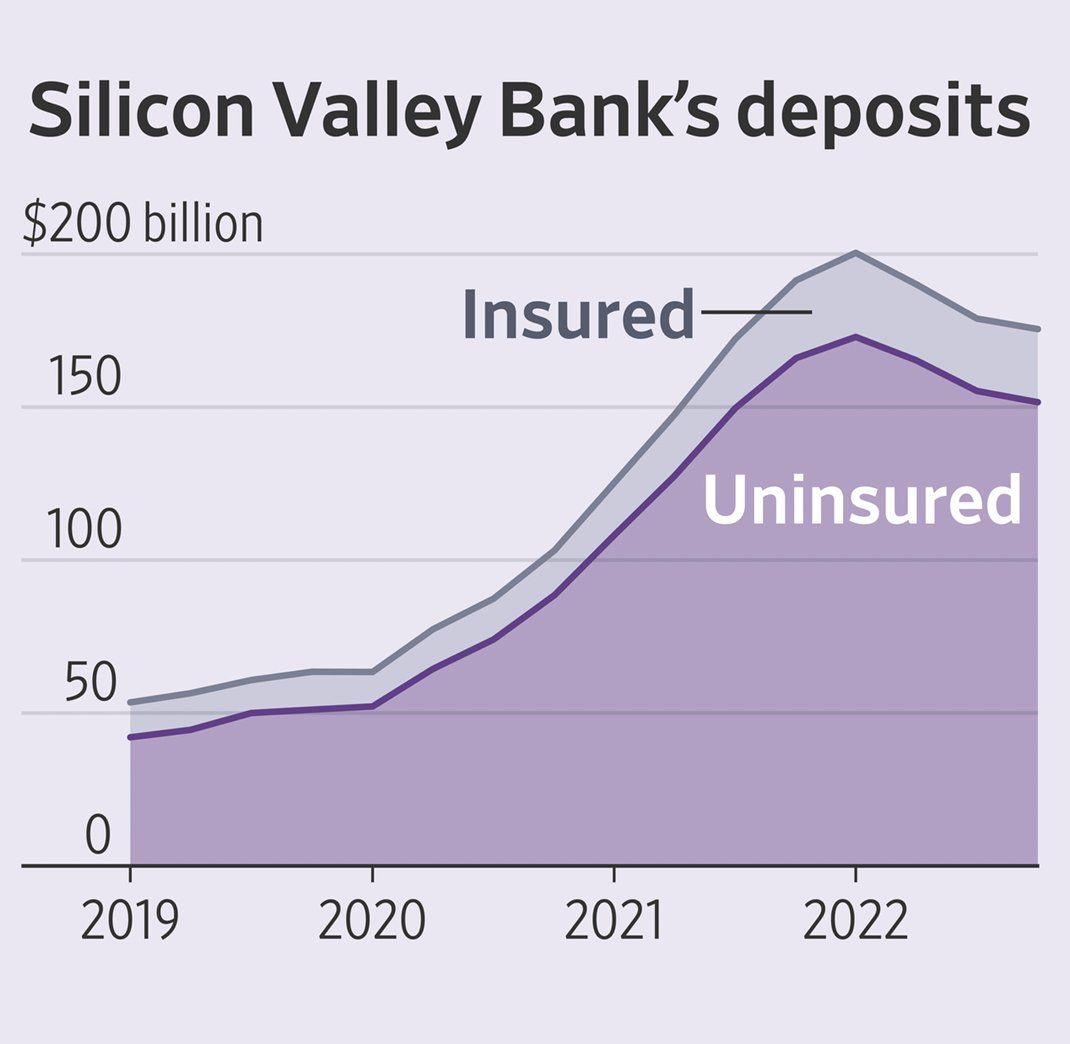

However, the collapse of Silicon Valley Bank and Credit Suisse magnifies the restrictive financial conditions created by the rate hikes and quantitative tightening that have already occurred. Deposit flight, a collapse in bond prices and banking sector stress - a consequence of rate hikes - are now influencing the future path of Fed policy.

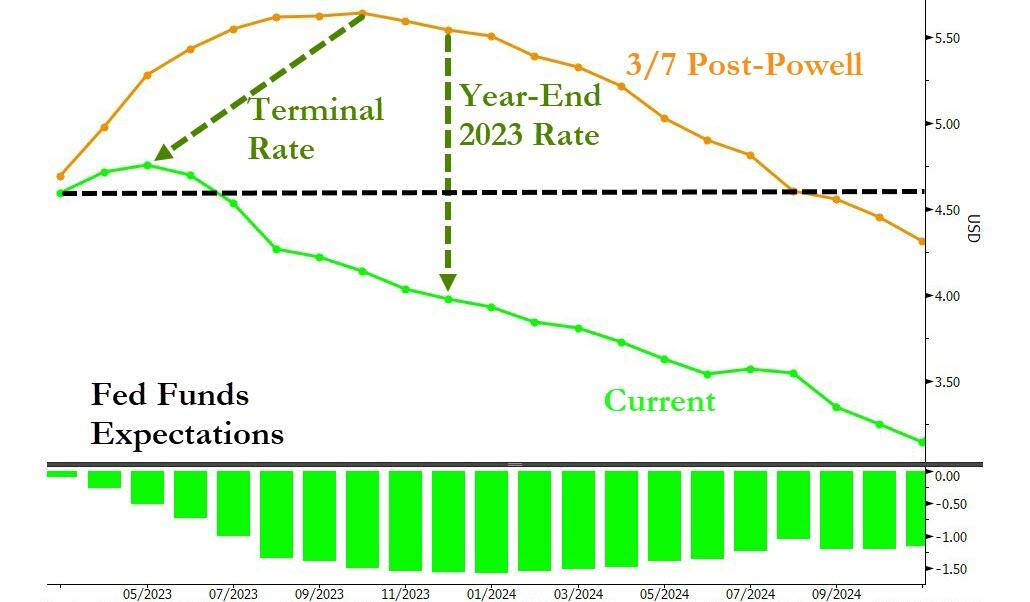

Interest rate markets are considering the possibility of a sharp contraction, and have significantly lowered forward projections for Fed policy rates. The problem is markets are anticipating a Fed reaction to something that has yet to happen.

True, we saw a few banks go down last week but for now the music is still playing. While there could be a financial crisis in the future, there currently is no financial crisis. So should Jay Powell scale back his well telegraphed fight against inflation to accommodate for the possibility of a banking crisis?

The question of the week is this: WTF is Jay Powell going to do and say this Wednesday?

He claims to be data dependent and has stated publicly that “a failure to restore price stability would mean far greater pain.” Well, the data (although backward looking) shows inflation is still too high while the economy remains relatively strong. In my opinion, it is likely he 1) raises by a compromising 25bps, 2) remains hawkish on inflation and 3) argues the banking crisis is contained.

Remember: although it has declined from the peak, as of the last release headline CPI is still 3x Powell’s target.